Central to the ISDA documentation architecture is the ISDA Master Agreement. The ISDA Master Agreement is the standard contract used to govern all over-the-counter (OTC) Derivatives transactions entered into between the parties. Transactions across different asset classes and products are often documented under the same agreement.

The purpose of the ISDA Master Agreement is to set out provisions governing the parties’ overall relationship. There are a number of different versions of the ISDA Master Agreement, including the 1992 and 2002 versions. The paper focuses on the 2002 version, but many of the concepts and issues discussed will be common across each of the different versions.

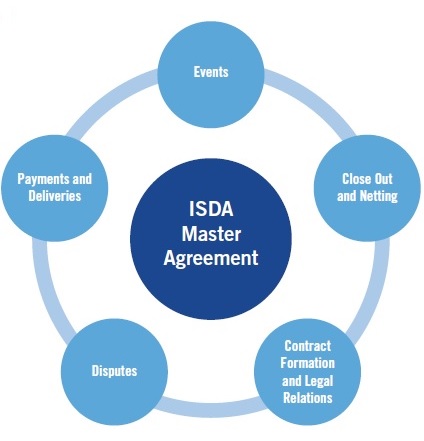

It is possible to break down the ISDA Master Agreement into five core themes (see below diagram).

- Events

In the context of the ISDA Master Agreement, this refers to things that happen outside the contract that may affect the parties’ respective ability to perform their obligations under their transactions. For more details, click here. - Payments and Deliveries

While the economic terms of a transaction are contained in the confirming evidence of that transaction – its confirmation – there are a number of provisions within the ISDA Master Agreement that may affect or modify both the quantum and timing of payments and deliveries and the manner in which payments and deliveries are made. - Close Out and Payment Netting

In certain scenarios, the parties may be entitled to terminate transactions entered into under an ISDA Master Agreement. The agreement outlines how the termination process operates.

Additionally, the ISDA Master Agreement contains important provisions to ensure that one party’s financial exposure to the other across all transactions is capable of being determined on a net basis. This has important benefits from a credit risk mitigation and regulatory capital perspective, and is a crucial element of the ISDA Master Agreement. - Legal Disputes

The ISDA Master Agreement establishes how the parties should resolve any disputes that might arise in respect of their overall trading relationship. - Contract Formation and Legal Relations

Beyond the four core areas outlined above, the ISDA Master Agreement also contains a number of provisions aimed at creating a legally effective and robust contractual relationship between the parties. These include provisions on how the contract might be amended, any representations made by the parties and how notices are effectively delivered.

- Occurrence of Events

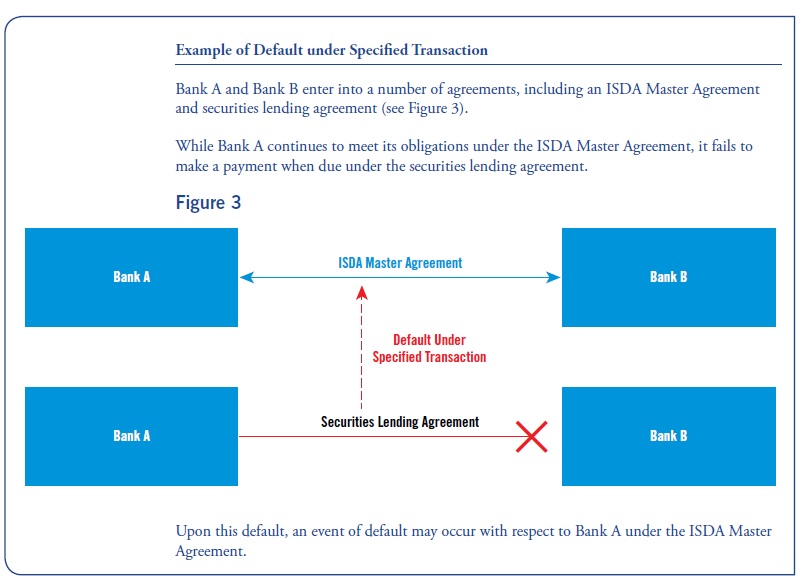

The ISDA Master Agreement provides for both events of default and termination events. Provisions relating to events of default and termination events are contained in section five of the ISDA Master

Agreement. Although the ultimate consequence of both is the same – the potential termination of a given set of transactions – they are conceptually distinct. Additionally, the mechanics and timing for determining when an event of default or termination event has occurred may differ depending on the nature and circumstances of a specific event.

Where an event contemplated by any of the events of default or termination events occurs, it does not necessarily mean any transactions will actually be terminated as a result.

Subject to some limited exceptions, events of default and termination events will only give rise to the right to terminate an ISDA Master Agreement (or certain transactions under an ISDA Master Agreement) once the non-defaulting or non-affected party delivers a notice of the relevant event to the other party. The process for terminating transactions under an ISDA Master Agreement is explained in more detail in the ‘Close Out and Netting’ section.

There are a number of scenarios where a party may not wish to close out an ISDA Master Agreement, even where an event of default has occurred. For example, if the close out would ultimately result in it having to make a sizeable payment to the defaulting party, then the non-defaulting party may not be inclined to exercise its right to terminate.

There are additional complexities involving the occurrence of events, relating to both timing and the scope of application. In some circumstances, the occurrence of the event will only constitute an event of default or termination event if certain additional steps are taken and/or a specified period of time elapses.

Grace Periods

Certain events of default can only occur once a specified grace period has elapsed. Grace periods therefore provide parties with an opportunity to remedy the issue that might otherwise give rise to an event of default.

Determining the duration of the grace period upon the occurrence of a particular event may not always be straightforward. Some grace periods use calendar days for determining their duration. Others are determined by reference to days on which commercial banks are open in a relevant jurisdiction in which the parties are located (defined in the ISDA Master Agreement as ‘local business days’).

The grace periods applicable to certain events of default may also be contained in other documents. For example, when considering whether a credit support default has occurred, it will be necessary to look at the terms of the relevant credit support document to confirm whether any grace periods might apply to performance of the relevant obligation.

Certain termination events (for example, illegality) may only occur after giving effect to any applicable fallback or remedy specified in a confirmation or elsewhere in the ISDA Master Agreement. This means that parties may be required to demonstrate they have taken all reasonable

steps to mitigate or cure the impact of the event prior to being permitted to terminate the ISDA Master Agreement (or certain transactions under it).

2. Payment and Deliveries

The economic terms of a transaction, including terms relating to payments and deliveries, are contained in the confirmation. References to payments in this section include (unless otherwise stated) reference to deliveries. A confirmation will set out how a payment amount is calculated, when it should be made and by whom, among other things.

A fundamental obligation of the ISDA Master Agreement is the requirement that parties should make payments to each other as and when due under their transactions. However, the performance of a payment obligation depends on the condition precedent in Section 2(a)(iii) of the ISDA Master Agreement being satisfied.

Section 2(a)(iii) stipulates that if a certain event with respect to a party has occurred (such as an event of default or a termination event), then the other party is not obliged to perform any of its obligations to make payments for as long as such event continues.

The obligation to make the payment is therefore ‘suspended’ for the duration of the event. In this scenario, it is important to note that, notwithstanding the existence of grace periods in respect of certain events of default, payments and deliveries are conditional upon no event of default or potential event of default having occurred and continuing. Therefore, where an event occurs that may at some point in the future constitute an event of default with respect to a party, the other party may suspend payment.

Interest and Compensation Payments

Where a payment is not made, whether because it has been deferred due to the operation of Section 2(a)(iii) (as discussed above) or because a party has defaulted, the ISDA Master Agreement provides for the payment of interest on these payments.

Depending on the scenario, the rate of interest payable will be determined differently, but as follows:

• Where a party has defaulted on payment, the interest rate applicable will be the payee’s cost of funding plus 1% per annum (defined in the ISDA Master Agreement as the default rate);

• Where a payment obligation is deferred due to the operation of Section 2(a)(iii), the interest rate applicable will be the rate at which the payer can borrow from a major bank in a relevant interbank market for overnight deposits (defined in the ISDA Master Agreement as the applicable deferral rate).

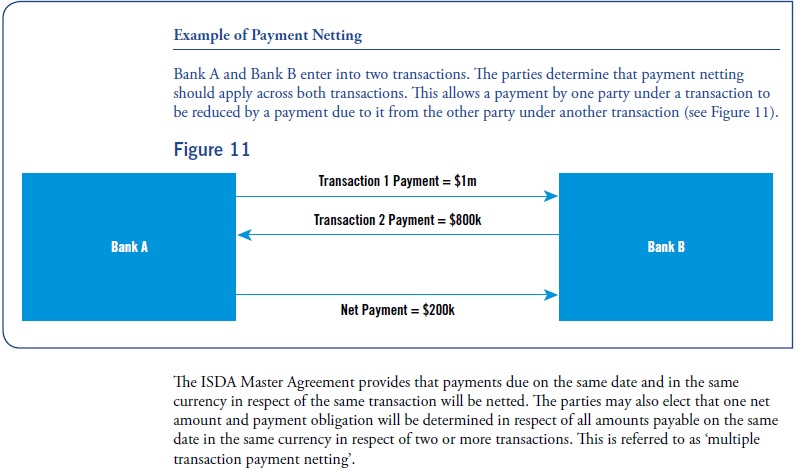

3. Payment Netting

Transactions entered into under an ISDA Master Agreement do not create separate and distinct contracts between the parties. Instead, they are incorporated by reference into a single agreement under the ISDA Master Agreement architecture. One of the benefits of the single agreement

architecture is the ability to net payment obligations arising under multiple transactions at the individual transaction level in order to determine a net amount that is payable at the ISDA Master Agreement level.

Netting takes two forms in the ISDA Master Agreement. Payment netting takes place during the normal business of a solvent firm, and involves offsetting cashflow obligations between two parties on a given day and in a given currency into a single net payable or receivable.

However, this is distinct from close-out netting, which applies to the netting of transactions when the ISDA Master Agreement is terminated or closed out due to the fact that one Counterparty is in breach of the Agreement.

CLOSE OUT AND NETTING

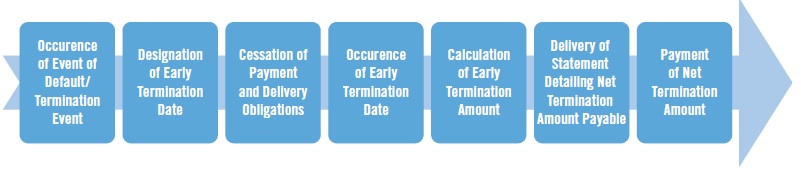

Upon the occurrence of an event of default or termination event, either party (or, in some scenarios, both parties) may have the right to terminate or close out transactions entered into under the ISDA Master Agreement.

The process of closing out or terminating transactions entered into under an ISDA Master Agreement involves seven steps or elements (see below diagram). Provisions relating to close out are found in Section 6 of the ISDA Master Agreement.

As part of the close-out process, all of the outstanding payment and delivery obligations of the parties with respect to terminated transactions are replaced with a single early termination amount due from one party to the other.

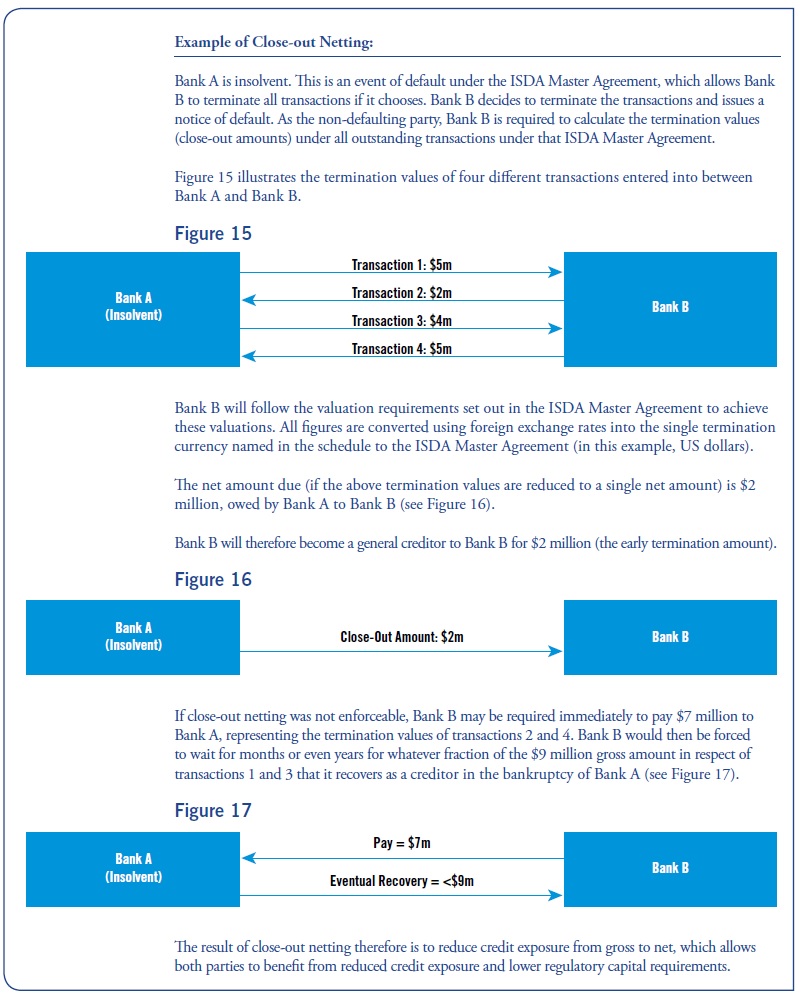

Close-out netting has advantages from both a credit and capital perspective. For example, when analyzing the amount of overall financial exposure that a party has to each of its counterparties, credit departments will typically do so based on the net exposure when a legally enforceable netting agreement is in place. From a capital perspective, regulated entities may be able to hold less capital if they are able to account for their exposures to their counterparties on a net basis.

However, in scenarios where one of the parties is insolvent, the close-out netting provisions of the ISDA Master Agreement may not always be enforceable due to the operation of insolvency law in the jurisdiction in which the insolvent party is based.

For example:

• Bankruptcy laws in certain jurisdictions may limit the availability of contractual set-off in an insolvency;

• Local insolvency laws might limit the effectiveness of contractual termination provisions when they are triggered on the basis of the opening of the insolvency proceedings;

• Under insolvency legislation, the liquidator may have the right to require the continuation or repudiation of transactions entered into by the insolvent party. This creates the risk of ‘cherrypicking’, whereby the liquidator could potentially decide to continue any valuable transaction

for the insolvent party while repudiating other transactions, therefore undermining the entire netting mechanism.

The close-out netting provisions of an ISDA Master Agreement will be considered to be enforceable where the effectiveness of these provisions in the event of a party’s insolvency are supported by a reasoned legal opinion in the relevant jurisdiction2. For example, when trading with a counterparty incorporated in and trading out of Germany, it will be necessary to procure a legal opinion affirming that the close-out

provisions of the ISDA Master Agreement will be legally enforceable under German insolvency law.

4. Legal disputes

At the transaction level, disputes may arise as a result of a disagreement over how a particular calculation was performed, for example. The manner in which a dispute is resolved with respect to an individual transaction may depend on the specific asset class being traded and the terms of the confirmation (as supplemented by asset-specific definitional booklets) entered into between the parties.

At the ISDA Master Agreement level, disputes may arise from events that are already anticipated by the standard events of default and termination events within the agreement. The effect of these events will generally be managed by the relevant mechanisms within the ISDA Master Agreement,

but might need to be resolved by negotiated settlement between the parties or in national courts or other dispute resolution venues.

Under the ISDA Master Agreement, the manner in which a dispute is ultimately managed and resolved is dependent on a number of factors, including:

• The governing law of the ISDA Master Agreement (generally either English or New York law);

• The facts and circumstances of the dispute;

• The parties’ relationship; and the terms of the ISDA Master Agreement with respect to the issue(s) in dispute.

Disputes may also arise from events that are not explicitly set out within the terms of the ISDA Master Agreement (for example, fraud or the application of sanctions or freezing injunctions), and may also arise before, during or after the lifecycle of a given transaction.

5. Contract formation

In addition to the obligations already discussed within these guidelines, the ISDA Master Agreement contains various other obligations with which parties must continuously comply while the agreement is in force. For example, it provides for an obligation to deliver any documentation

specified in the schedule to the ISDA Master Agreement at certain intervals or upon request. This typically includes any tax forms needed to enable a party to make payments to the other without any tax withholding, copies of constitutional documents, signing authority and financial statements.

These obligations are not transaction-specific and must be adhered to throughout the duration of the legal relationship between the parties, irrespective of the nature of any transaction entered into or, indeed, whether or not any transactions have been entered into at all.

Provisions relating to agreements between the parties are primarily found in section 4 of the ISDA Master Agreement.

Source: www.ISDA.org