Project finance related transactions are very special and complex deal structures, whereas they are even in some cases conducted by specialized organizations, like for instance Czech export Bank. Involving of such institution is necessary whenever the financing activities and their purpose is to support the export of complex technology or equipment abroad, while there is certain element of Government subsidizing to partially repay the loans. Such projects are naturally done through big ticket deals when it comes to construction of Hydro-plants, Wind farms, Energy power-plants, Steel processing lines, Gas extraction plants, Water sewage system etc., so that the Creditor faces significant risks especially in delivery and implementation phase of financed equipment.

Such projects are very demanding on proper assessment and analyzing the following:

a) Counterparty risk – whether Borrower is depending on state subsidies or is generating income on open market

b) Country risk – what are the conditions for getting all necessary approval for running installed technology and equipment, what are the limitations in Profits distribution

c) FX risk – to hedge against unexpected shortfalls in receiving cash from running production facilities to repay the loan due to changed local currency rates

d) Funding risk – whether the Sponsor(s) is/are enough credible to provide Own Equity into the Project

e) Completion/ Construction risk – relevant for General constructor who will be responsible for putting the imported technology into the running mode without defects; and others.

Speaking about all the afore mentioned risks, then appears to be evident that such projects are pretty close to Insurance of receivables, which is also covered by EGAP and another commercial insurance entities in Czech Republic. For more details, please refer to Section Off B/S financing.

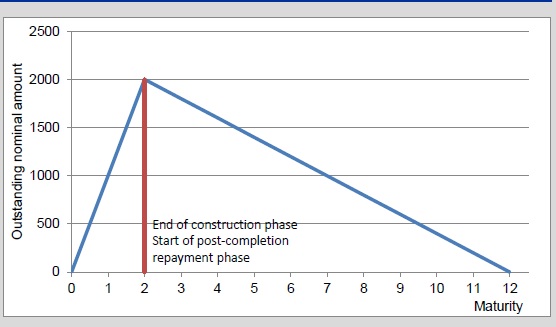

Very often these projects are turned into LT-Investment financing, when the completion stage is finished, as repayment of the loan is scheduled into LT-amortization profile depending on the ability to generate Cash flow purely from installed facility. Therefore, in financial assessment the Banks usually separate the Object of financing from other business activities of the Borrower and Debt service is matched only to Income from Project, itself.

According to Article 147(8) of the CRR, project finance loans possess the following characteristics:

(a) the exposure is to an entity which was created specifically to finance or operate physical assets or is an economically comparable exposure;

(b) the contractual arrangements give the lender a substantial degree of control over the assets and the income that they generate;

(c) the primary source of repayment of the obligation is the income generated by the assets being financed, rather than the independent capacity of a broader commercial enterprise.

As mentioned above, an important feature of project finance is that these loans are primarily recovered from the income of the project. Project finance is used for the financing of long-term infrastructure, industrial projects and public services, where project debt and equity used to finance the project are primarily paid back from the cash flow generated by the project. An important feature of project finance is that the structure and funding of the project are tailored to the project’s specific characteristics. Therefore, in practice many solutions are possible, so that different products can be used, with different terms and conditions applicable to each one.

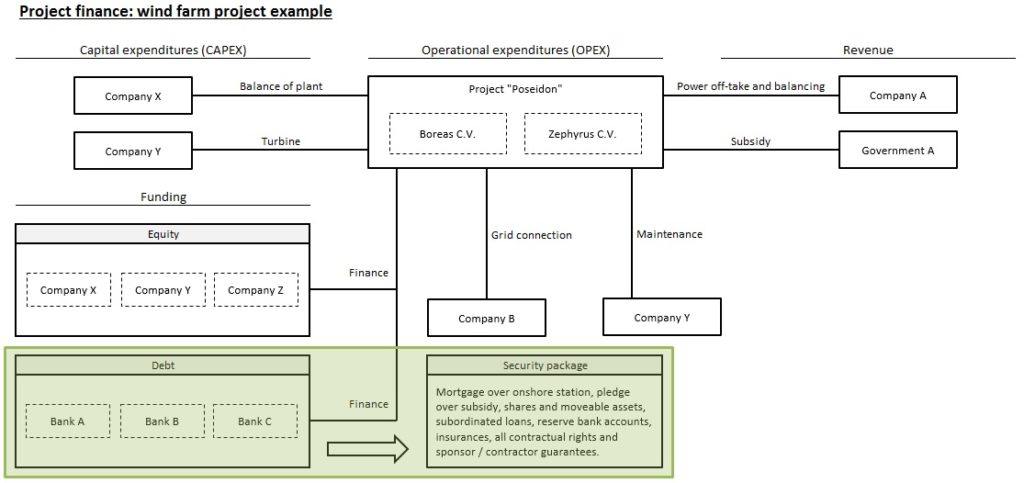

For an illustration of a project finance structure, please consider the following example.

The project – called “Poseidon” – is a well-defined ring-fenced project with several owners (also called sponsors or investors). The project contains several special-purpose vehicles (SPVs) and is controlled by an independent board (project group).

Ring-fencing the project means that the project company and all the assets and liabilities will be connected to the project, and the project company is not allowed to be involved in other business transactions (such as borrowing in order to purchase other assets not connected to the project). Ring-fencing a project without establishing a legal entity solely for the purposes (SPV) of the project is hardly possible.

In this case, the SPVs have the legal form “Joint-venture”. The managing partners in the company are responsible for the debt of the company. The so-called silent partners (or Sponsors) provide equity and are – on the condition that they do not interfere in the management of the company – responsible for the investment which they have made. Managing partners are severally liable so that they all remain as joint Co-Borrowers until the full Debt repayment.

In this project – in which an offshore wind farm is built – company X and company Y are actually building the wind farm. These companies (called contractors) are delivering respective parts to the Project construction and are responsible for the maintenance of the wind farm. For that they need to get paid, which will be secured firstly from Own funds contribution (by Companies X, Y and Z), while the substantial part will be funded from Banks external funds. After the completion, Company B will be responsible for maintaining the connection into the Grid network and obtaining all licenses for running this facility, but the Fixed assets purchased and completed will be owned by Boreas C.V. and Zephyrus C.V. (under SPV structure).

The (future) revenues of the project are generated by selling the power to company A and partially from subsidies provided to the project by Government A. No other income is expected at level of these SPV entities running the Project Poseidon.

That’s in line with the main premise in project finance, that the structure has been set up with one specific goal only: to carry on activities solely for the purpose of the project. This means that the SPVs are not expected to engage in any business areas not serving the purpose of the project.

As these types of transactions are very close to LT-Investment facilities, the Banks have usually the same approach to financing structure, which is fully “ring-fenced” with following assets to be pledged:

- General Pledge of trade Receivables and stocks

- Mortgage on Fixed assets subject to Financing

- Pledge of current Accounts

- Parent company guarantee

- Insurance policy for Real-estates immobilization

- Subordination of I/C loans

- Commercial insurance covering Performance and Warranty Bond, Costs-excess, Country and political risks etc.

Usual documentation type to be signed with Client:

- Project financing Loan agreement (based on LMA standard)

- Agreement on pledge of trade Receivables and stocks

- Pledge of current Accounts Agreement

- Mortgage agreement on Fixed assets subject to Financing

- Pledge agreement on SPV business shares

- Insurance policy for Real-estates immobilization agreement

- Subordination of I/C loans agreement

- Performance and Warranty Bond

- Commercial insurance policy immobilization agreement

The Project finance facility is usually supported by additional financial covenants like:

- Solvency ratio (min. 15% depending on the business industry of Borrower), calculated as Tangible Net Worth / Total Assets

- Interest coverage ratio (ICR) to be at least 1.5x which is calculated as the ratio of EBIT/Interest costs during the Construction period

- Debt service coverage ratio (DSCR) to be at least 1.20x which is calculated as the ratio of EBITDA/ total Debt service (Principal + Interest costs) during the Investment period

- Maximum Leverage ratio to be capped at 4.0x which is calculated as the ratio of total Bank Debts/ EBITDA

- Dividends restriction until the acceptable level of the loan is repaid (e.g. 50%)

- And others depending on Project assumptions and agreed structure.

Each Project finance case is very specific, so that the collateral structure and covenants stipulations may differ case by case, nevertheless this particular description of Project Poseidon depicts most usual contractual obligations and arrangements, which every financing Bank and Project counter-party must take into account when analyzing each Project.

source: www.ECB.europa.eu