This article will guide you through upcoming changes in regulatory area focused primarily on capital and other prudential ratios designed by European regulatory frame-work and inspired by Basel capital accords. Most recent updates will actually materialize in modified CRD and CRR measures, which will be able to tackle the potential risks in financial industry and to make the banks and other organisations better equipped and prepared against them.

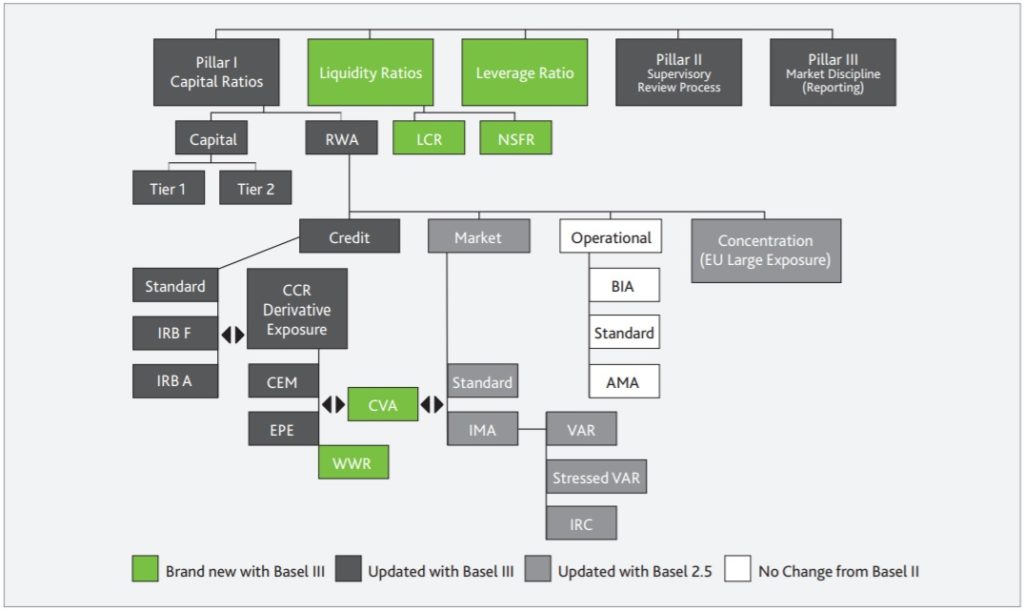

Afore mentioned diagram summarizes overall structure of major ratios, that were subject to latest Basel reforms and other connected regulations adopted by EU (like CRD and CRR). As there is certain overlay in those requirements, let’s make short introduction and update on these measures for financial sector.

The difference between Basel and CRR/CRD

Quite clearly, the new Basel III regulations will affect all banks globally, however the severity of the impact will differ according the type, scale and location of banks. Vast part of (commercial) banks will be impacted by the increase in quantity and quality of capital, liquidity and leverage ratios (within pillar 1), as well as the enhanced requirements for pillar 2 and capital preservation. In addition, most sophisticated investment banks will be affected by the amended treatment of counterparty credit risk, the more robust market risk framework and to some extent, the amended treatment of securitizations. On top of that, Global Systemically Important Banks (G-SIBs) are subject to higher core tier 1 capital requirements.

For instance, the US financial sector has been implementing Basel III, under the auspices of the Dodd-Frank Act, since 2015. It covers almost all banking institutions and closely mirrors the BIS framework, with modifications that met the requirements of the US regulators. However, the usage of liquidity ratios in the US is still under review. A complexity for US banks is that banks must also manage their stress testing alongside their Basel III compliance, under the Comprehensive Capital Analysis and Review (CCAR) and the Dodd-Frank Act stress test (DFAST) frameworks. This presents a challenge as a bank’s Basel III results need to be consistent with the stress testing results.

The overarching goal of the Basel III agreement and its implementing act in Europe, the so-called CRD IV package, was meant to strengthen the resilience of the EU banking sector to be better placed to absorb economic shocks, while ensuring that banks continue to finance economic activity and growth. In 2013, the European Union adopted a legislative package to strengthen the regulation of the banking sector and to implement the Basel III agreement in the EU legal framework. The new package replaces the current Capital Requirements Directives (2006/48 and 2006/49).

The Capital Requirements Regulation (CRR) contains the detailed prudential requirements for credit institutions and investment firms while the new Directive (CRD) covers areas of the current Capital Requirements Directive where EU provisions need to be transposed by Member States in a way suitable to their respective environment. The package applies as of 1 January 2014. Some of the new provisions have been phased-out between period of 2014 to 2019.

So, did CRD IV and CRR fully implement “Basel III” principles?

EU has actively contributed to developing the new capital, liquidity and leverage standards in the Basel Committee on Banking Supervision, while making sure that major European banking specificities and issues are appropriately addressed. The new rules therefore respect the balance and level of ambition of Basel III. However, there are two reasons why Basel III cannot simply be replicated into EU legislation:

1) Basel III is not a law. It is the latest configuration of an evolving set of internationally agreed standards developed by supervisors and central banks. That has to go through a process of democratic control as it is transposed into EU (and national) laws, as it needs to fit within existing EU (and national) laws or arrangements. Nevertheless, consequence of not complying with Basel standards in case of Capital adequacy for instance would be rather a reputation issue for bank, as it would influence external rating assessment and position of the bank on capital markets (as an Issuer of own Bonds for instance). While on the other hand, failing with CRD and CRR rules could trigger a process of revoking the banking license.

2) Furthermore, while the Basel capital adequacy agreements apply to “internationally active banks”, in the EU it has always applied to all banks (more than 8,300) as well as investment firms. This wide scope is necessary in the EU where banks that are authorised in one Member State can provide their services across the EU’s single market and as such are more than likely to be engaged in cross-border business. Also, applying the internationally agreed rules only to a subset of European banks would create competitive distortions and potential for regulatory arbitrage. The EU has had to take these circumstances into account when transposing Basel III into EU law.

Below attached diagram shows entire set of currently discussed regulatory topics in financial segment, world-wide:

What is Europe adding to “Basel III”?

In addition to Basel III implementation, the proposal introduces number of important changes to the banking regulatory framework.

For instance, within CRD, you can find among others:

- Enhanced transparency – more details needed to be disclosed regarding the activities of banks and investment funds in different countries, as concerns profits, taxes and subsidies in different jurisdictions.

- Systemic risk capital buffer – Each Member State may introduce a Systemic Risk Buffer of Common Equity Tier 1 for the financial sector or one or more subsets of the sector, in order to prevent and mitigate long-term non-cyclical systemic or macroprudential risks. Until 2015, in case of buffer rates less than 3%, Member States did not need prior approval from the EU Commission. From 2015 onwards and for buffer rates between 3 and 5 % the Member States setting the buffer will have to notify the Commission, the EBA, and the ESRB. The Commission will provide an opinion on the measure decided. And any buffer above 5% need to be confirmed by EU Commission and legally ratified by respective Member state.

- Global systemic institution (“GSII”) capital buffer – This buffer is mandatory for banks that are identified by the relevant authority as “global systemically important institutions” to compensate for the higher risk they pose to the global financial system and for potential impact of their failure.

- Other systemic institution (“OSII”) capital buffer – The capital requirements directive IV provides for a buffer to include domestically important institutions as well as institutions of EU importance. For instance, in case of the Czech banking sector, banks like Ceska sporitelna, Komercni banka, CSOB, Raiffeisenbank, PPF Banka and J&T Banka were recognized as being “OSII”.

- Countercyclical capital buffer – part of a set of macroprudential instruments, designed to help counter pro-cyclicality in the financial system. Capital buffer should be accumulated when cyclical systemic risk is judged to be increasing; Czech National Bank set this reserve at 1,75% since January 2020 for banks acting in CR.

- Remuneration – from 2014 onwards, the variable component of the total remuneration shall not exceed 100% of the fixed component of the total remuneration of material risk takers (in order not to accept higher risks/larger volumes just to reach higher salary).

- Enhanced governance – strengthening the requirements regarding corporate governance arrangements and processes and introduces new rules aimed at increasing the effectiveness of risk oversight by Boards.

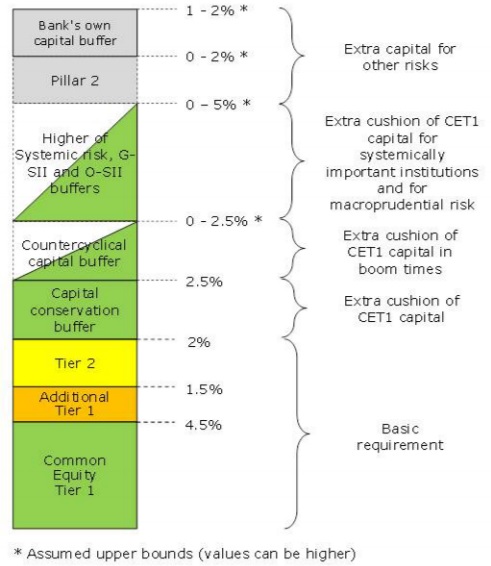

Below attached is the overview of Basel III capital structure requirements, that has been almost entirely adopted by CRD Directive, as well:

Within the CRR, there is also included:

- A “single rule book”: For the first time a single set of harmonised prudential rules is created which banks throughout the EU must respect. This will ensure uniform application of Basel III in all Member States, and thus remove a large number of national options and discretions from the CRD, and allows Member States to apply stricter requirements only where these are justified by national circumstances (e.g. real estate), needed on financial stability grounds or because of a bank’s specific risk profile.

Upcoming changes in the prudential framework regarding credit institutions in EU

a) CRD 5 – DIRECTIVE (EU) 2019/878 as of 20 May 2019 amending Directive 2013/36/EU representing updated and modified CRD IV directive:

- The transposition deadline of CRD5 – until 28.12.2020 (that is, the Czech Parliament must approve the directive)

- The application of the transposed provisions – most of the provisions to be applied from 29.12.2020 as follows: (i) from 28.6.2021 – the new regulation assessment of interest rate risk in the investment portfolio, adjusting the criteria for the supervision and evaluation proces resp. (ii) from 1.1.2022 – restrictions on own funds allocation in the event of failure to fulfil the capital reserves to the leverage ratio for GSIIs.

b) CRR2 – REGULATION (EU) 2019/876 as of 20 May 2019 amending Regultion (EU) No. 575/2013 representing updated and modified CRR regulation:

- most of the provisions to be applied from 28.6.2021 retroactively from January 2019, exceptions to deductions of capital investments (especially with insurance companies);

- Implementation of new BCBS (Basel Committee on Banking supervision) standards: (i) Net stable funding ratio – the primary goal is to ensure that financial institution has an acceptable amount of stable funding to support the institutions assets and activities over the medium term (over a 1 year period) etc. (ii) Leverage ratio – defined as Tier 1 capital divided by a measure of non-risk weighted assets as to bring institutions’ assets more in line with their capital in order to help mitigate destabilising deleveraging processes in downturn situations (iii) a revised market risk concept (iv) a new standards for disclosure of information;

- new provisions on Total loss absorbing capacity (TLAC) standards to be yet defined following the changes in the resolution framework; currently G-Sibs are required to hold a TLAC amount of 16% in terms of risk-weighted assets (RWAs), or 6% of the leverage exposure measure. This is most likely to increase up to 18% of RWAs, resp. 6.75% of leverage exposure by January 1, 2022. Instruments that count as TLAC need to be able to be converted into equity (like subordinated debts, senior debt notes, convertible bonds etc.) to recapitalise the entity, in order to avoid to pass losses onto investors and minimise the risk of a government bailout;

- approval of parent holding entities;

- the principle of proportionality;

- categories of institutions – in terms of their importance, size, interconnectivity and complexity to be divided into subcategories as follows: (i) large institutions, (ii) small and not very complicated institutions and (iii) other institutions; such categorization is critical to determine capital requirements for disclosure, reporting and applied ratios like NSFR etc.

- Change in capital reserves and Pillar II

- Other changes proposed in area of credit risk, renumeration, reporting etc.

Prudential consolidation

- change in scope – always the responsibilities of the parent company;

- the parent entity includes the subsidiaries, which is either an (i) institution (ii) financial institution or (iii) ancillary services undertaking;

- still prevails so-called CRR consolidation vs. accounting consolidation (IFRS).

Article 18 (7) CRR2

- Where an institution has a subsidiary, which is an undertaking other than an institution, a financial institution or an ancillary service undertaking or holds a participation in such an undertaking, it shall apply to that subsidiary or participation the equity method. That method shall not, however, constitute inclusion of the undertakings concerned in supervision on a consolidated basis.

- By way of derogation from the first subparagraph, competent authorities may allow or require institutions to apply a different method to such subsidiaries or participations, including the method required by the applicable accounting framework, provided that: (a) the institution does not already apply the equity method as of 28 December 2020; (b) it would be unduly burdensome to apply the equity method or the equity method does not adequately reflect the risks that the undertaking referred to in the first subparagraph poses to the institution; and

- (c) the method applied does not result in full or proportional consolidation of that undertaking.

Categorization of institutions according to CRR2:

- Large institution based on Article 4/(146) of CRR meeting any of the following conditions:

- it is a G-SII or O-SII (Global or Other systemic important institutions);

- it belongs to the one of the three largest institutions in terms of total value of assets (in the Member State in which it is established);

- the total value of its assets on an individual basis or (where applicable), on the basis of its consolidated situation in accordance with this Regulation and Directive 2013/36/EU is equal to or greater than EUR 30 billion;

Small and non-complex institution means an institution that meets all the following criteria:

- it is not a large institution;

- the total value of its assets on an individual basis or, where applicable, on a consolidated basis in accordance with this Regulation and Directive 2013/36/EU is on average equal to or less than the threshold of EUR 5 billion over the four-year period immediately preceding the current annual reporting period; Member States may lower that threshold;

- it is not subject to any obligations, or is subject to simplified obligations, in relation to recovery and resolution planning in accordance with Article 4 of Directive 2014/59/EU;

- the total value of its derivative positions held with trading intent does not exceed 2% of its total on- and off-balance-sheet assets and the total value of its overall derivative positions does not exceed 5%, both calculated in accordance with Article 273/a(3);

- more than 75% of both the institution’s consolidated total assets and liabilities, excluding in both cases the intragroup exposures, relate to activities with counterparties located in the European Economic Area;

- the institution does not use internal models to meet the prudential requirements in accordance with this Regulation except for subsidiaries using internal models developed at the group level, provided that the group is subject to the disclosure requirements laid down in Article 433a or 433c on a consolidated basis;

- the institution has not communicated to the competent authority an objection to being classified as a small and non-complex institution.

New goals regarding regulatory reporting areas according CRR2

Article 430 (8) off CRR2 – for EBA issue of adequacy:

- classify institutions into categories based on their size, complexity and the nature and level of risk of their activities;

- measure the reporting costs incurred by each category of institutions during the relevant period to meet the reporting requirements;

- make recommendations on how to reduce reporting requirements at least for small and non-complex institutions.

The development of a consistent and integrated system for collecting statistical data, resolution data and prudential data:

- EBA shall prepare a feasibility report by June 2020

- When drafting the feasibility report, EBA shall involve competent authorities, as well as authorities that are responsible for deposit guarantee schemes, resolution and in particular the ESCB.

- The report shall take into account the previous work of the ESCB regarding integrated data collections and shall be based on an overall cost and benefit analysis, including.

Implementation of revised Basel III in EU

Revision as of December 2017, mainly focused on:

- review of credit risk and operational risk measurement;

- adjustments of CVA risk measurement (so banks can use either the standardized approach (SA-CVA), which now requires a supervisor’s authorization, or the basic approach (BA-CVA));

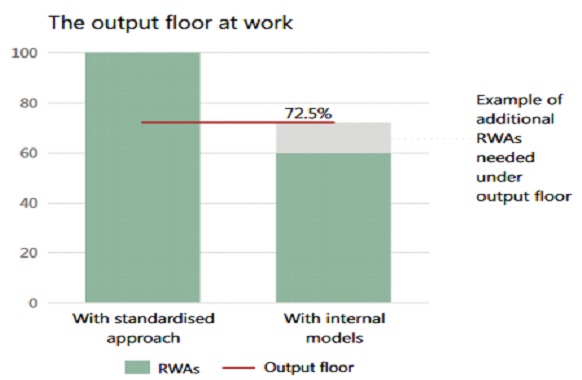

- replacement of Output floor definition based on Basel III standards (Standardized approach); in general, Output floor was set to limit the benefits that banks can derive from using internal models to calculate minimum capital requirements. For instance, Banks’ calculations of RWAs generated by internal models cannot, in aggregate, fall below 72.5% of the risk-weighted assets computed by the standardised approaches. This limits the benefit a bank can gain from using internal models up to 27.5%, only.

- Focus on Standardized approach again in more areas

- Leverage ratio – changes relates to G-SIB (Globally Systemic Important Banks);

- restrictions on approaches based on the application of the Pillar 1 model: (a) IRB restrictions (credit risk) and (b) removing the AMA (operational risk);

- by the year 2022 changes in credit risk, operational risk, market risk, CVA, Leverage ratio will be applied;

- 2022 – 2027 output floors (commencing at 50% in 2022, phase-out to final 72.5%), refer below for details:

However, no consensus was achieved on the treatment of sovereign risk, and more time was allowed for the review of the market risk framework. All these proposed changes and updates are still subject to local codification and may undergo final “fine-tunning” as a reaction on latest market trends, which are hard to be foreseen upfront.

The full version of mentioned CRD Directive and CRR regulation is herewith attached:

sources: https://ec.europa.eu/commission/presscorner/detail/en/MEMO_13_272, www.bis.org, ww.risk.net, www.bankovnictvionline.cz, www.moodysanalytics.com, www.esrb.europa.eu/national_policy/ccb/html/index.en.html,