Trade finance products have developed throughout the time in order to match with trading habits mainly in export business, however they needed certain “golden rules” that would be applicable for all trading partners, for all commodities and under all jurisdictions. This is given the international aspect of foreign trade, so that it is exposed to unknown trading partners with very weak business history or experience and even the Banks found it very risky and difficult to finance such activities.

Therefore, International Chamber of Commerce (ICC) came up in 1936 with very first set of The Incoterms rules that were accepted by all governments, legal authorities, and business partners involved in international trade. They were intended to reduce or remove altogether uncertainties arising from differing interpretation of the rules in different countries. As such they have been regularly incorporated into sales and financing contracts. This had huge impact on current conditions of trade structuring, as the uncertainty has not been totally removed from business presence, it was just eliminated via using the Trade documentation (like Trade L/C) in confirming the delivery of the goods into pre-agreed place, quantity and time, so that the Buyer/Seller will avoid the risk of non-delivering/non-paying for it. In certain simplification it can be said, that the Banks (and Buyers) are not willing to honor the Seller by means of “Clean payment” for agreed commodity while not having in hands any ownership title documentation.

Letter of credit (L/C) is representing most usual payment tool in foreign trade business area securing the rights of all participants, whereas the Seller is guaranteed to receive the purchase price while the Buyer will obtain the ordered goods for his payment.

Naturally, the Bank is entering into this transactions and guarantees the proper settlement of the deal, as it has contractual obligation to check the presented documents that were specified in purchase contract, to verify their correctness and completness and to release the purchase price against these documents, so that ownership rights transfer from Seller onto Buyer is well managed.

From technical perspective, the Banks and financial community have developed during the time secured communication channel TELEX, which was used for sending the encrypted messages between the Banks. This has been further replaced by SWIFT, which is more reliable and user-friendly, so that the whole proces of sending the underlying documents for L/C deals became trusty-worth. In fact, proper type and form of SWIFT message sent by Bank to its counterparty represents confirmed commitment without any further needs to verify correctness of such statement.

The Bank has in fact critical role in this business relationship, as it acts like an intermediary agent and clearing entity, so it has obligation to act independently. When trying to find an analogy in lending business, Trade L/C is similar to Escrow Account agreement, which also defines precise conditions and circuimstance, under which the Bank is obliged (and must) to pay out the stipulated money. The payment under the Trade L/C is de-facto opposite to clean payment, where just invoice is issued and payment must be performed. Typical Trade L/C, when is issued, includes main parameters like specification of the goods, purchase price, presentation date, shipment date, expiration date etc.

So that, the Seller and Buyer must agree prior to L/C issuance, where the goods is supposed to be handed-over and what corresponding documents will be accompanying the goods delivery. Based on that, the Bank (of a Buyer) will issue Trade L/C, confirming that purchase price will be honoured in case that all required documents will be presented. Those documents typically include following:

- Invoice and Tax declaration (if applicable)

- Bill of landing, Airway bill, Railway receipt etc. depending on selected way of transportation

- Insurance certificate (if applicable)

- Origination certificate, Inspection certificate etc.

The scope of those documents resp. required conditions to be met are specified under the INCOTERMS stipulations (like FOB, CIF, EXW etc.), which means that Bank must apply those general rules when controlling the presented documents in order to decide whether they are fully compliant or whether there is any discrepancy found. In case that no discrepancy was claimed, that means that Seller (Beneficiary) has fulfilled his obligations and Buyer (Applicant) must pay. If the Buyer became meanwhile insolvent, then the Bank of the Buyer (that has issued L/C) must remit the agreed price, which is the most important aspect of documentary business, that the payment risk is fully transferred onto the Issuing bank, which normally has some external credit rating. Based on that the Seller receives very solid assurance that Buyer can not fully default on his payment duty.

In the practice life, there are various variations/forms of Trade Letter of credits, which may be as follows:

- Deffered L/C: the payment terms are deffered and L/C is due within 90 days after presenting the documents

- Stand-by L/C: quasi an Performance bond securing that Beneficiary gets paid after the Aplicant fails to pay; this is in contrast to usual Trade L/C, where it is honoured after all arrangements were properly made and documents presented

- Confirmed: when another Bank confirms the already issued L/C, it means that it has also joint obligation with issuing Bank to pay

- Transferrable: when a Beneficiary agrees that his rights to be honoured can be partially or fully transferred onto another Beneficiary (applicable for sub-deliveries trade structure etc.)

- And others.

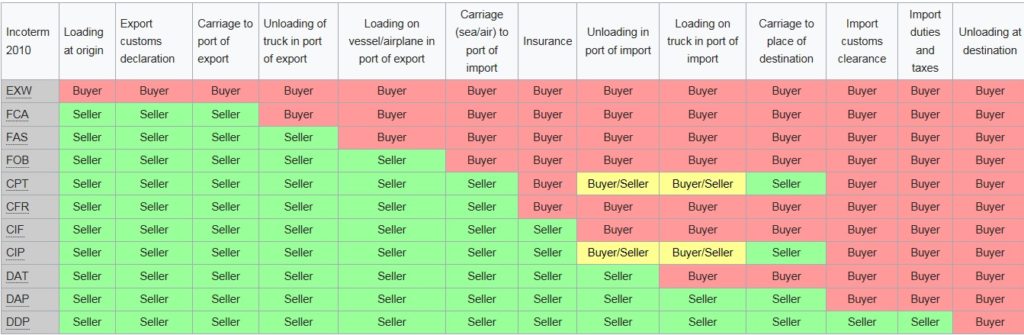

The overview of all INCOTERMS Conditions applied in Documentary financing is shown below:

International Chamber of Commerce (ICC) has issued the restated rules under INCOTERMS 2010 valid since January 2011 providing better classification for all delivery rules and their harmonization as total number of these rules was reduced from 13 to 11. This was achieved via replacing previous DAF, DES, DEQ and DDU with DAT and DAP, that are now applicable for all kind of transportation.

The summary of restated rules

1st sub-group of Delivery rules/ conditions represents rather more universal category, which is applicable for all means of transportation and even for a combination of different means. These are EXW, FCA, CPT, CIP, DAT, DAP and DDP.

EXW – Ex Works represents most favorable delivery condition for Seller, as he is obliged to deliver the ordered goods just to his own sales premises or warehouse, while the Buyer undertakes all remaining risks including the loading of the goods, transportation, customs duty and insurance costs. Given this, this condition is recommended to be used rather in domestic trade, as there is limited (practically to zero) duty of Seller to provide necessary cooperation for tax and customs administration. And in case of any heavy goods, that needs better loading equipment, it is more useful to adopt FCA condition, so that Seller will have to carry the loading activity on Truck, train or ship (on his own costs).

FCA – Free Carrier is an alternative for EXW, but tailored for international trade, whereas the delivery place is specified to be still in the premises of Seller, but his condition includes to load and deliver the goods to transportation company and to present all documents needed for customs (export) regime, so that the goods can freely cross the borders. Nevertheless the Seller is not obliged to pay the import tax and customs in country of Buyer.

CPT – Carriage paid to enables certain flexibility in delivering the goods (and transferring the ownership and risks connected to that) in specific point of destination, usually that is derived from changing the transportation company or vehicle, so that the Seller carries all connected risks up to handing over the goods to the first transportation company (based on his own selection). Likewise in case of FCA, the obligation of Seller is finished with securing required documents for free export.

CIP – Carriage and Insurance Paid to condition is enhancing the obligation of Seller by additional requirement for securing the insurance of goods (against damage or loss) during transportation up to the place of delivery, however the place for delivery must be properly specified to be sure where is transfer of risks/costs taking place.

DAT – Delivered at Terminal resp. DAP – Delivered at Place are representing more convenient conditions for Buyer, as the Seller must deliver the goods to any nearest Port of Airport, from which the goods will cross the border either by sea, rail or air. Further, the Seller must properly arrange the transportation to this Port including the loading from/onto respective boat, train or airplane. Naturally, the obligation of Seller is finished with securing required documents for free export.

DDP – Delivered Duty paid is clearly the best solution for Buyer in international trade, as the Seller carries all risks and costs connected with delivery of the goods, even his obligation is also to declare the goods and cover import taxes and customs fees. In case that customs duty should be borne by Buyer then DAP rule was supposed to be applied.

2nd Subcategory of delivery rules/ conditions is applicable mostly for sea/water transportation, as there are included direct stipulations that are relevant mostly for Boat as a transportation vehicle.

FAS – Free alongside the ship is describing that Seller`s obligation ends-up with placing the goods next to the Ship at the Port, whereas in case of goods packed in the container this is supposed to be taken-over at handling station located in the Port, so that FCA condition will be rather applied. The damage and loss risk of the goods is also handed-over from Seller to Buyer after deploying the goods along the Boat in the Port.

FOB – Free on Board condition is just minor deviation from FAS as the goods is expected to be placed directly on the board of the Ship instead of along the Ship. In addition, as the Goods is already loaded onto the transportation vehicle, that may transport it across the borders, the Seller must also conduct export customs administration.

CFR – Costs and Freight means the obligation of Seller to deliver the goods on Boat and to pay all corresponding costs for transportation up to the Port of Buyer, where the goods will be taken over. However regarding the damage/ loss risks, these end up with loading of the goods onto the Board, but in case of Boat accident, the damage costs are born by Buyer. Given the different places of ownership and responsibility transfer, it is highly recommended to cover all potential situations in purchase agreement on top of Incoterms stipulations.

CIF – Costs, Insurance and Freight is possible to agree in trade relations only in case that Buyer has strong negotiation power, so that Seller accepts to cover all costs connected with delivering the goods up to the Port of targeted country and this is even including the insurance costs during the transportation. The point for handing-over the goods from Seller to Buyer is supposed to be Buyer`s port, so that this requires very good specification of this place to fulfill the conditions of purchase contract.

Sources: www.Businessinfo.cz, www.wikipedia.org, www.ICCwbo.org