Traders buy and sell financial products. As a result they often have positions or exposures. These exposures can arise because they are speculating or they have simply hedged against the other side of trade with client. Whatever the reason as prices move the market value of these positions will change.

This means that movements in foreign exchange rates, interest rates, credit spreads and commodity prices lead to profits and losses. All these situations are part of market risk, because they have been triggered by movement of market prices for underlying asset class. One of the most popular methods of measuring market risk is Value at Risk, (VaR).

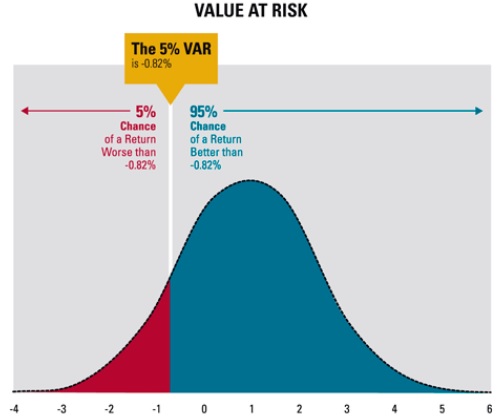

Value at Risk tells you how much money you can lose over a given time period and for a given level of confidence from the positions you hold. But it is not a guaranteed maximum loss figure. Your positions could lose you a lot more than VAR indicates, in the end.

Sometimes markets move by huge amounts in very short space of time. As a consequence your dealing positions can give you losses much greater than the VaR you have calculated.

Value at Risk is measured in either (i) price units or as (ii) a percentage. This makes the interpretation and understanding of VaR relatively simple. Further, Value at Risk is applicable to all types of assets like Bonds, Currencies, Interest rates, Commodities etc. Therefore, this advantage make it so widely used, as it is accepted standard in buying, selling or investment recommendations for all assets. However, VAR does not deal with option positions very well. It also does not measure operational risks.

Four main factors influence your VaR number, they are:

- Exposure: In general the larger the position you have the greater the risk. Therefore large positions create greater VaR.

- Time: The longer you intend to hold the position the greater the VaR. As you may expect 10 day VaR is greater than 1 day VaR. (But not by a factor of 10, only the square root of 10).

- Confidence: If you want a VaR that is very unlikely to be exceeded you will need to apply more stringent parameters. All things remaining constant this will increase your VaR and make it less likely to be exceeded.

- Volatility: If you deal in risky things that have a history of going up and down in price, or if market conditions alter to make your positions move up and down in price your VaR will tend to increase.

It is important to put any VaR number you see into context. This means that if you are provided with a VaR number you should also know:

- What is the probability that it will be exceeded?

- What is the holding period?

Many firms do not solely rely on VaR to manage market risk. They use a variety of measures that may include traditional techniques like basis point value and stress testing. Stress testing shows what can happen when extreme market moves arise. It focuses attention to what can happen when markets move abnormally. You can see what a bad day could really cost you. By using several measures banks are looking for consistency in the reporting of risk. It is like having a second, third and fourth check on VaR.

In financial markets diversified asset portfolios are generally considered to be less risky than undiversified portfolios nad thus limitating the potential losses incurred on one title with Profits generated by another title. This is for instance pretty much close to concept of Pension/ Investment Funds assets allocation, as they generally set firm rules ufront, what can be share of one title within the overall Portfolio (e.g. up to 2% for Investment grade rated corporate shares). This simple rule will then help to protect the whole Portfolio against sudden losses made by one or couple of more shares, unless the whole market undergoes serious (down-side) correction.

When risk managers calculate VaR they can provide you with both figures, undiversified and diversified value at risk. Diversified VaR takes into account the portfolio effect, which is important. It means in theory that adding products can lead to changes in the VaR that are not as great as you may anticipate.

In general, regulators are supportive for using the VaR. Many Banks in cooperation with their Auditors have agreed with the regulator the use of VaR in order to calculate market risk and therefore the amount of regulatory capital required to support it. But, then the VaR model needs to be an accurate assessment of the risks the Banks run. Therefore if you expect your VaR to be exceeded only 1 day in 100 days, your regulator will not appreciate a frequency that exceeds this. It would indicate that your VaR model is inaccurate and your regulator may decide to increase the amount of regulatory capital you are holding.

Example:

Suppose the Bank has purchased a Government bonds in total value of USD 10 Mio that have a actual price of 100 (resp. at Paar value) and based on historical experience the daily price volatility is rather limited, so less than 0.5%. And using statistics, (standard deviation, SD), there is following scenario most likely:

- 84.1% chance (1day SD), that the Bonds price tomorrow will not fall below 100 – 0.5% = 99.50,

- 97.7% chance (2days SD), that the price tomorrow will not fall below 100 – 1% = 99.00 and

- 99.8% chance (3days SD), that the price tomorrow will not fall below 100 – 1.5% = 98.50.

This example literally describes the usual “behaviour” of Bonds, which probability or a chance of gradual collapse of these instruments three days in a row is pretty much reducing from initial 15,9% (resp. 100% – 84.1%) to 0.2% (100%-99.8%), which represent solid confidentiality level. Put it another way, you are 99.8% sure that in normal market conditions your loss on holding this asset for three days will not exceed 1.5%, (resp. USD 150,000 on a USD 10 Mio position), this is the VaR. If the Bank buys a more risky security, say one with a daily volatility of 1% your three days VaR for a 99.8% confidence interval is 3%, resulting to maximum loss of USD 300,000 from same position. Therefore, the increased historical volatility, the increased VaR, in general.

Conclusion:

So, what confidence interval and holding period should be used? That is entirely up to each Banks management decision. In determining the time horizon it is usually considered how long it could take to liquidate open positions. Many banks use between 5 and 10 days with a 2 or 3 standard deviation confidence interval. It just depends on how conservative your regulator (and Auditor) risk measures want to see.

source: www.investopedia.com