IFRS 9 is the International Accounting Standards Board’s (IASB) response to the financial crisis, aimed at improving the accounting and reporting of financial assets and liabilities. IFRS 9 replaces IAS 39 with a unified standard. The mandatory effective date for implementation is January 1, 2018. IFRS 9 introduces changes across three areas with profound implications for financial institutions:

- Classification and Measurement: IFRS 9 introduces a logical approach for the classification of financial assets driven by cash flow characteristics and the organization’s business model in which an asset is held. This principle-based approach replaces existing rule-based requirements which are complex and often difficult to apply.

- Impairment: Under IFRS 9, the expected credit loss (ECL) model will require more timely recognition of credit losses compared with the incurred loss model of IAS 39. The new standard requires entities to account for expected credit losses using forward-looking information and lowers the threshold for recognition of full lifetime expected losses.

- Hedge Accounting: IFRS 9 represents a substantial overhaul of hedge accounting that aligns the accounting treatment with risk management activities, enabling entities to better reflect these activities in their financial statements.

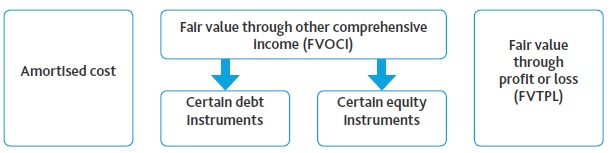

Classification of assets

With the adoption of IFRS 9, the usual classification of assets is supposed to be changed, while former Assets Groupping based on IAS 39 (Held to maturity, Trading assets etc.) has been replaced with a new one, as the primary key is an obejctive of relevant Business model, and this is determining factor for a valuation method of their fair value and how they are recognized in the accounting. Newly proposed Groupping consist of following classes:

- Assets and debt instruments measured at amortised costs – financial asset must be in a „Hold to collect“ (HTC) business model. That is, an objective to collect the contractual cash flows from the financial asset (interests) rather than with a view to selling the asset to realise a profit or loss (from different purchase/sale price). But, there is a specific exception where financial assets may be sold as a result of an increase in the assets’ credit risk. Typically such assets are for instance Loan receivables with ‘basic’ features, Investments in government bonds that are not held for trading, Investments in term deposits at standard market interest rates etc.

- Investments in debt instruments resp. Shares measured at fair value through other comprehensive income (FVOCI); which is de-facto into Equity funds. This business model typically involves greater frequency and volume of sales than the HTC business model. Integral to this business model is an intention to sell the instrument before the investment matures. These assets may include Government/ Corporate bonds, where the Bank has clear intention that the investment period is likely to be shorter than final maturity. On the contrary, it is unlikely that intercompany loans or trade receivables would be classified in the FVOCI category.

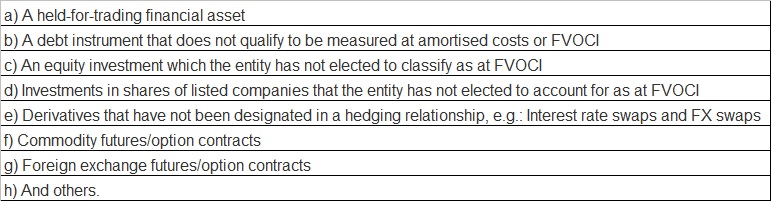

- Financial instruments that are measured in Fair value through Profit/Loss Statement are mainly represented by Derivatives that were previously recognized under “Held for trading” category, but also encompass the residual part of Investments that simply did not fit into previous categories. Almost complete list of these financial asset includes:

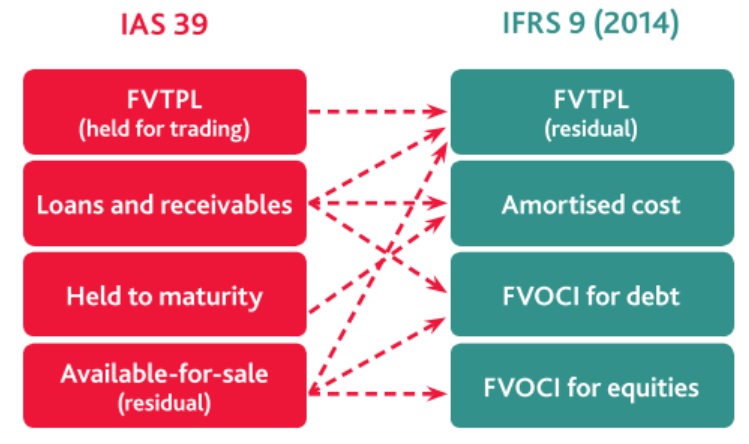

The movement (adjustments) in between of individual classes categories can be also for better understanding depicted in line with following diagram:

IFRS9 Impairment methodology

Replacing IAS 39 with IFRS 9 will significantly impact banks’ financial statements, the greatest impact being the calculation of impairments:

- IAS 39 – A provision is made only when there is a realized impairment. This results in “too little, too late” provisions and does not reflect the underlying economics of the transaction.

- IFRS 9 – Aligns the measurement of financial assets with the bank’s business model, contractual cash flow characteristics of instruments, and future economic scenarios. Banks may have to take a “forward-looking provision” for the portion of the loan that is likely to default, even shortly after its origination.

From credit risk point of view, the main area that has been changed by new IFRS 9 rules is Impairment methodology, which now newly requires from the Banks to work more actively with current credit Portfolio data and to foreseen the future development of entire Portfolio based on certain behavioural statistics as well as in the context of local economy environment.

Key drivers that will in the end translate into modified Impairments/ECL have been defined as following:

It will no longer be necessary for a credit event to occur before credit losses are recognized. The measurement of allowance of credit loss will depend on the instrument’s impairment stages.

An entity will be required to base its assessment and measurement of expected credit losses on historical, current, and forecast information that is available without undue cost or effort. Measurement of financial assets will be aligned with a bank’s business model, contractual cash flow of instruments, and future economic scenarios.

The forward-looking provision framework will make financial institutions evaluate how economic and credit changes alter their capital and provision levels at each subsequent reporting date.

For instance, see below attached simulation, how ECL may finally differ given the different macro-economic conditions on local market:

Quite clearly, economics down-turn (Scenario 3) accompanied with lower GDP growth, higher Unemployment and stagnating housing market will result into higher ECL when compared with stable market conditions (Scenario 1) and that represents one of the main drivers for Provisioning policy, which was so far according to IAS 39 relatively static and almost zero effort of the Banks was spent on foreseeing any future development that could signifficantly influence the final result of Defaulting the client on its Debts.

Main areas of impact:

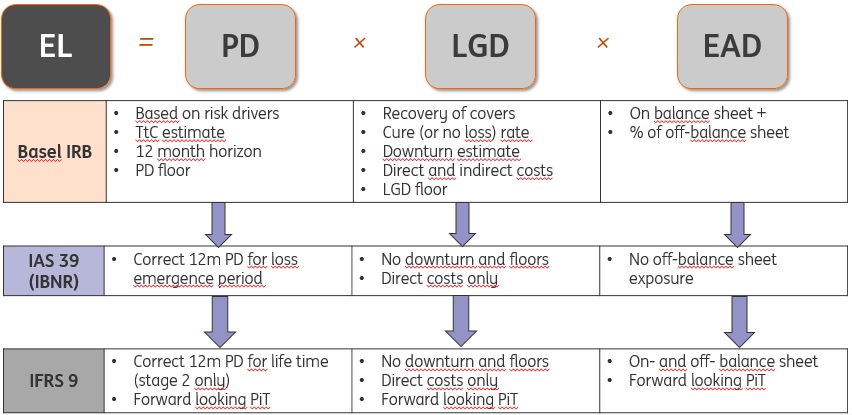

- ECL calculation engine: The calculation engine will need to be robust and flexible. It will need to incorporate facility-level and be adjusted by credit events. The ECL engine will need to support granular calculations and expected modeling challenges. It must have built-in data quality checks and reports, and must be able to define or choose ad hoc economic forecast and scenarios. It must be capable of modeling or importing PD, LGD, and EAD term structures and behavioral metrics affecting cash flows. It must be able to allocate, optimize, and value collateral and credit risk mitigants. The standard way, how ECL is derived from those three afore mentioned elements, is shown below at diagram at the bottom of this text.

- Impairment calculation: Institutions must have the ability to calculate a probability-weighted impairment that incorporates past events, current conditions, and forecasts of future economic conditions. In addition, valuation analysis needs to consider scenario-specific cash flows. In the end, IFRS 9 adoption will affect the Banks profitability via impairment costs incurred within Profit and loss statement.

- Reporting and financial statements: It will be necessary to reconcile with other regulatory rules, including Basel 3, the Dodd-Frank Act, and the Foreign Accounting Tax Compliance Act (FATCA). Institutions will need to reconcile risk and finance data where risk data will be used down to the legal reporting entity level.

- General ledgers reconciliation: Ledgers will need to reflect IFRS 9 calculations and new impairment metrics. Financial institutions usually have several general ledgers within a single legal entity. Computational and performance requirements: The IFRS 9 forward-looking impairment calculation will require higher volumes of data than the current IAS incurred loss model, Basel guidelines, or stress testing. Institutions will want to do facility-level analyses, and calculations leveraging scalable architecture, such as grid computing processes, will be imperative.

- Collateral allocation and valuation: Institutions will need to determine how to incorporate collateral effects on the valuation and computation of cash flows for impairment calculation purposes.

- And many others.

For instance, Moodys Analytics made an research within the Banking industry on how the adoption of IFRS 9 will be embraced by the financial institutios and whether this is deemed only as additional burden or the opportunity for improvement. Below attached see the results of this research:

As conclusion out of that, vast part of respondents considered the IFRS 9 implementation as serious challenge into their in-house processes, more than 80% were planning to have Parallel run (of IAS 39 and IFRS 9) in place for a transition period, some of the even budgeted some extra costs to be allocated for higher compliance and as a result, after securing higher granularity for analysis, better allignment with BASEL infrastructure should be achieved in the end.

Credit Staging

Impairment of loans is recognised, whether on an individual or collective basis, in following stages under IFRS 9:

- Stage 1 – When a loan is originated or purchased, ECLs resulting from default events that are possible within the next 12 months are recognised (12-month ECL) and a loss allowance is established. Interest revenue is calculated on the loan’s gross carrying amount (that is, without deduction for ECLs). In determining whether a significant increase in credit risk has occurred since initial recognition, a bank is to assess the change, if any, in the risk of default over the expected life of the loan (that is, the change in the probability of default, as opposed to the amount of ECLs).

- Stage 2 – If a loan’s credit risk has increased significantly since initial recognition and is not considered low, lifetime ECLs are recognised. The calculation of interest revenue is the same as for Stage 1.

- Stage 3 – If the loan’s credit risk increases to the point where it is considered credit-impaired or In default, interest revenue is calculated based on the loan’s amortised cost (that is, the gross carrying amount less the credit loss Provisions). Lifetime ECLs are recognised, as in Stage 2.

Based on this description above, Stage 1 and Stage 3 represent quite clear Stances of credit portfolio, which is then either Standard (1) or simply In default (3). Stage 2 represents certain transition stance between Standard and Defaulted loans, and this re-classification from Stage 1 to 2 makes happen when for instance:

- Lifetime PD has increased

- LGD re-calibration took place (reflecting the collateral valuation method adjustment)

- Forbearance status of Client has changed (due to Arrears on Payments being more than 30 Days overdue or Fin.covenants relaxation etc.)

- Client was assigned to Watch list (based on internal Rating deterioration by three Notches for instance) etc.

Quite naturally, the Stages (2-3) are directly connected with higher requirement for provisioning, so that this will have impact into Earnings results, however it must be seen in broader context that Regulators wish to see the Banks to be better prepared and equipped with sufficient Reserves (and Capital) for potential quality deterioration of their Credit portfolio.

Conclusion

Under the IFRS 9 ‘expected loss’ model, a credit event (or impairment ‘trigger’) no longer has to occur before credit losses are recognised. A financial entity will now always recognise (at a minimum) 12-month expected credit losses in profit or loss going forward. Lifetime expected losses will be recognised on assets for which there is a significant increase in credit risk after initial recognition.

The IASB’s project was initially carried out as a joint project with the US Financial Accounting Standards Board (FASB). However, the FASB ultimately decided to make more limited changes to the classification and measurement of financial instruments and the hedge accounting model, and to develop a more US specific impairment model for financial assets. The FASB’s ‘current expected credit losses’ model requires the recognition of the full amount of expected credit losses upon initial recognition of a financial asset.

Below attached is the complete guidance on Financial instruments and their recognition according to IFRS 9 as published by BDO:

source: www2.deloitte.com, www.bdo.global, www.moodys.com, www.iasplus.com, www.ifrs.org