Derivatives section will guide you through the sophisticated world of trades on Financial markets in order to understand their obvious structures, practical usage and documentation that is needed to be concluded for avoiding the main risks. When it comes to Derivatives, these are used mainly to hedge against following risks:

- FX (foreing currency movement) risk

- IR (interest rate movement) risk

- Commodity (price movement) risk.

Speaking about FX derivatives for instance, we must recognize that utilisation of Delivery limit is depending on two factors:

- Specific Currency pairs like EUR/USD, EUR/CZK, USD/CZK, USD/CHF etc., the risk weights for specific pairs is given by their historical volatility which is higher with emerging markets currencies (PLN, HUF, RUB etc.);

- Tenor of the deal, while simple rule is valid that the longer the tenor of the deal is, the higher risk weights are applied.

In general: EUR/USD Deal for 1 Month would result to <5% risk amount from total nominal amount of the deal. This would lead to utilization of Pre-Settlement limit on counteparty. This is needed to measure all the time in order to be able to monitor potential breaches on limits utilisation, plus in addition to properly assess the required collateral value so that the opened risk position is herewith reduced.

The Lehman Brothers’ bankruptcy made the entire trading community more sensitive to the need to protect collateral. So called independent amounts often turned out to be “commingled” with other assets or re-used by their prime broker. Clients who did not safeguard collateral with a third-party custodian realised how vulnerable those assets were. According to the ISDA survey, large dealers ’rehypothecated’ 73,6% of collateral.1

Therefore it has emerged as primary mitigant to protect against future losses from trading to have properly conducted Master agreement including CSA to manage cash margining and limitations in open positions.

Today, the bilateral agreement adopted between two counterparties dealing OTC derivatives is typically the master agreement published by the International Swaps and Derivatives Association (ISDA). It is composed of several components:

a) Master agreement: defines the general terms and conditions that will guide the relationship (obligations, events of default, governing law, payment netting etc.)

b) Schedule: adapts the Master Agreement to specific needs of the parties and sets out any particular terms the parties agree will apply to transactions between them

c) Conformation: sets out the term of a specific transaction

d) Credit support annex/CSA: relates to the financial collateral that will be exchanged between the parties (eligibility, frequency of margining, haircuts, thresholds).

The EMIR reforms will add to these documentation requirements. Clients will now have to sign one or more clearing agreements that bring into effect an additional agreement such as an ISDA master agreement with a collateral annex for cleared transactions.

Transactions will continue at present to be entered into directly between the client and the clearing member (or executing broker, under a give-up relationship). Once the clearing broker has entered into or accepted the transaction with the client, an equivalent transaction must also be registered in the client account of the clearing member at the clearing house. Of course, all this comes on top of the master agreement with the executing broker.

This is backed up with security interest in favour of the client over the receivable on that client’s account with the clearing house.

This is designed to mitigate client’s credit risk to the clearing member under the cleared ISDA agreement and cleared credit support annex (CSA). It does not, however, extend to any exposure under the existing non-clearing ISDA and CSA, or indeed to any other relationship between the client and the clearing member.

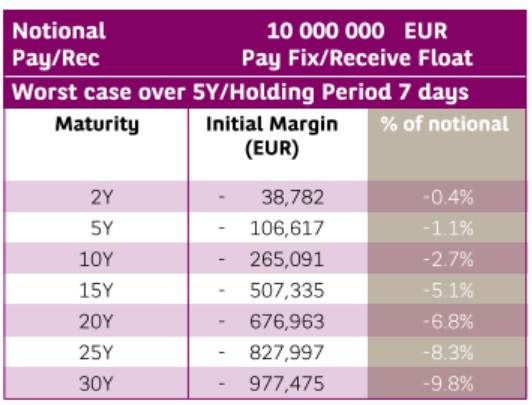

For instance, below atttached diagram shows the required Initial margin to be deposited with Central Depository for concluded Interest rate swap (IRS) for notional amount of EUR 10 Mio for tenor up to 30 Years. This requirement may lead to required deposit of almost EUR 978 tsd., representing nearly 10% of the Deal amount. 2 This also illustrates, how huge, could be also the loss from opened position for such deal. Thus it is not worth to underestimate those risks.

However, Collateral management (in form of Credit Support Annex) is also beneficial to initial credit approvement of trading limits, as it substantially decrease utilisation of risk weights for traded Derivatives. Each product bears different risk weights depending on tenor of the deal, underlying market risk (FX, IR or commodity) and currencies that are subject to exchange.

Unlike the standard credit risk, whereas the notional amount of the credit transaction requires the same approved limit, so that transaction can be concluded, in case of Derivatives the approved limit does not equal to notional deal amount, but only to risk amount, which is divided into:

- Delivery (or Pre-Settlement) risk and

- Settlement risk.

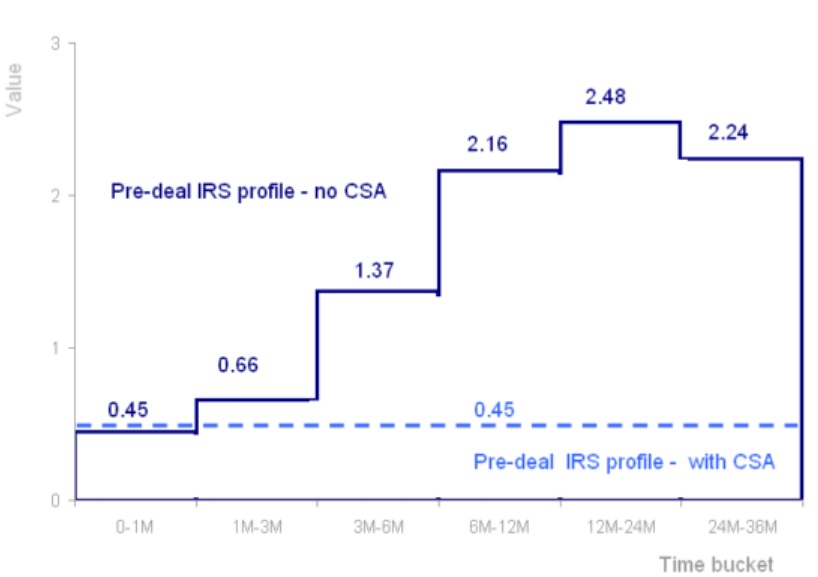

In general, Delivery risk (some institutions call it Pre-Settlement risk) reflects the situation that Counterparty defaults during the life-time of Derivative and cannot settle the deal at maturity. And therefore the Bank will be exposed to open position and thus will (i) suffer a loss on the outstanding financial contract with this Counterparty equalling to the positive Mark to Market (MtM) value and (ii) will have to close it on the market under current conditions. Nevertheless the risk weight for these Deals in only a fraction of the notional amount (e.g. from 5 to 20%). This can be even further reduced with signed Credit Support Annex (CSA), whereas margining mechanism should not allow the Counterparty to fall in deeper loss below the concluded threshold. For illustration see below attached diagram for utilisation of Delivery limit for IRS deal with and without an CSA agreement:

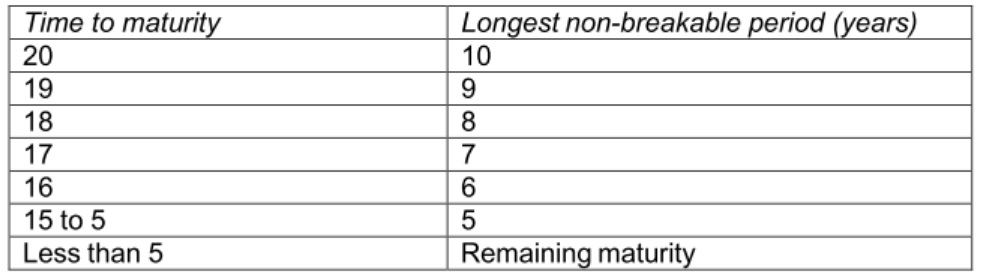

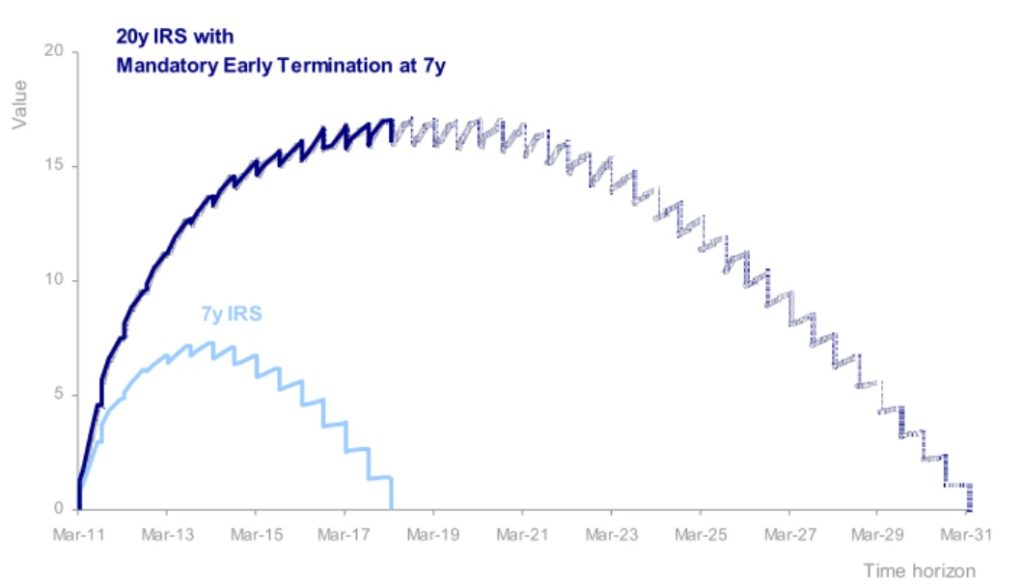

Further, for a long-term Deals (usually over 5Y), Break clauses are a means of mitigating credit risk by allowing the Bank to terminate a transaction on pre-determined dates, with the effect of shortening the tenor to which the Bank is legally committed in a transaction. The Exposure Calculation approach for trades with break clauses is identical to normal trades, but the period of exposure is shortened, which leads in general to reduction in Delivery Risk. Below attached are two diagrams showing the usual tenors for Break-clauses and respective utilisation of Delivery limit with and without mandatory Break clause after 7 Years (for 20 Years deal).

On the contrary, Settlement risk means a negative scenario that countervalue from concluded deal is not simply settled at maturity date from various reasons and mainly as the settlement takes place based on different Cut-off times for different currencies or products, the Bank may be exposed to risk that it has already sent out the funds in CZK while it has not yet received the countervalue in EUR (and may not receive it on same day due to operating issues etc.). This potential situation may be solved through Payment after delivery (PAD) clause, which secures that outcoming funds will be released from the Bank after the incoming funds have been received. In case of securities trading, the equivalent of this clause is Delivery versus payment (DVP). Otherwise, the Settlement risk equalls to 100% of deal notional amount.

Sources: www.ISDA.org, www.bnpparibas.com, www.investopedia.com

References: 1/ ISDA Margin Survey, published in April 2011 2/ BNP Paribas research publication “OTC Derivatives – The challenge of deriving clear benefits”, published in November 2016