Following the financial crisis in US (2008), the Federal Reserve Bank (FED) opted to save the faltering financial sector with guaranteed liquidity, so that it basically intervened on opened market via reducing refinancing market rates, based on which FED is providing the Banks with short-term funds.

This programme was conducted by Mr. Bernanke, beeing a FED chairman until his very last period in the office, and was labeled as QE – Quantitative Easoning. This was meant to describe the ongoing policy of sustaining very low interest rates, so that the economic growth can be supported from financial sector via providing new loans to economy and businesses.

As Mr. Bernanke was replaced in his office by a new Chairman, Mrs. Yellen, and the macro-economy indicators were showing good signs of stability and overall growth (unemployment rate fell to around 5%, Inflation rate fell below 2%, Building/housing permits have stabilized, Retail sales have been picking up) the official FED policy started to be more hawkish (in terms of tightenning the monetary policy) by means of increasing the market rates.

Almost at the same time, the Eurozone started to face a repeated decline in inflation rate, indicating that the economy was going towards a deflation. Responding to this threat and to re-build the market confidence and stability, the ECB has basically inspired itself from previous FED policy and announced in September 2014 the launch of following Asset purchases programmes (APP):

- the third Covered Bond purchase Programme (CBPP3)

- Corporate sector purchase Programme (CSPP) – Corporate bonds

- Public sector purchase Programme (PSPP) – Government bonds

- Asset-Backed Securities Programme (ABSPP) – Mortgage bonds

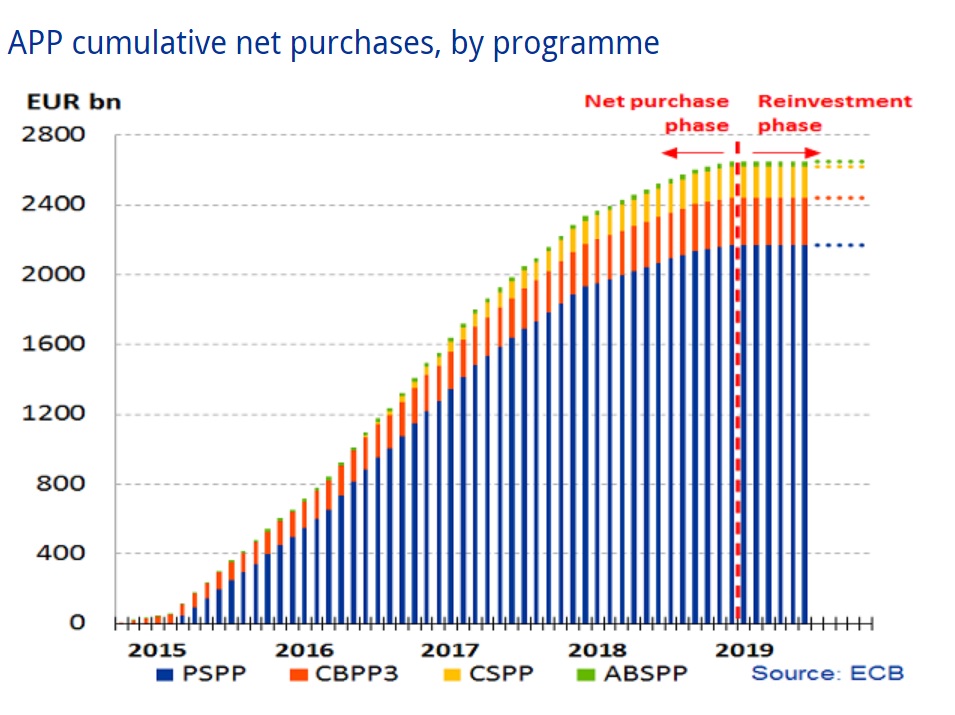

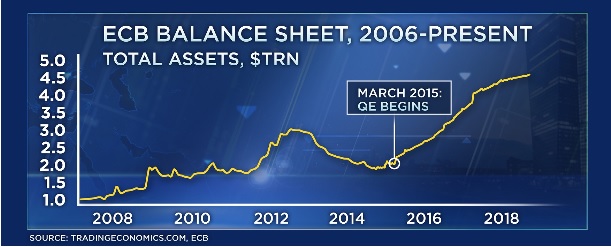

From above attached chart, it is clear that ECB has targeted within its APP the purchase of Government bonds issued by EU member countries reaching almost 80% of entire position. An extension of those programmes within a full-fledge “quantitative easing” programme which mainly included sovereign bonds, to the tune of 60 billion euros per month was put in place since March 2015. The program was repeatedly extended to reach about €2,600 billions and was initially expected to last until end of 2018. In connection with this, the ECB Balance sheet has increased from around € 2 trillion in 2015 to almost 5 trillion in 2018.

When ECB’s governing council announced the expanding quantitative easing programme (QE) to be muted in December 2018, it marked a historic moment for the central bank, as President Mario Draghi dismantled one of his most contentious policies. Only a couple of months later, first questions on future direction of monetary policy led by ECB started to pop-up on surface.

The market consequences of QE in most recent period have been notable:

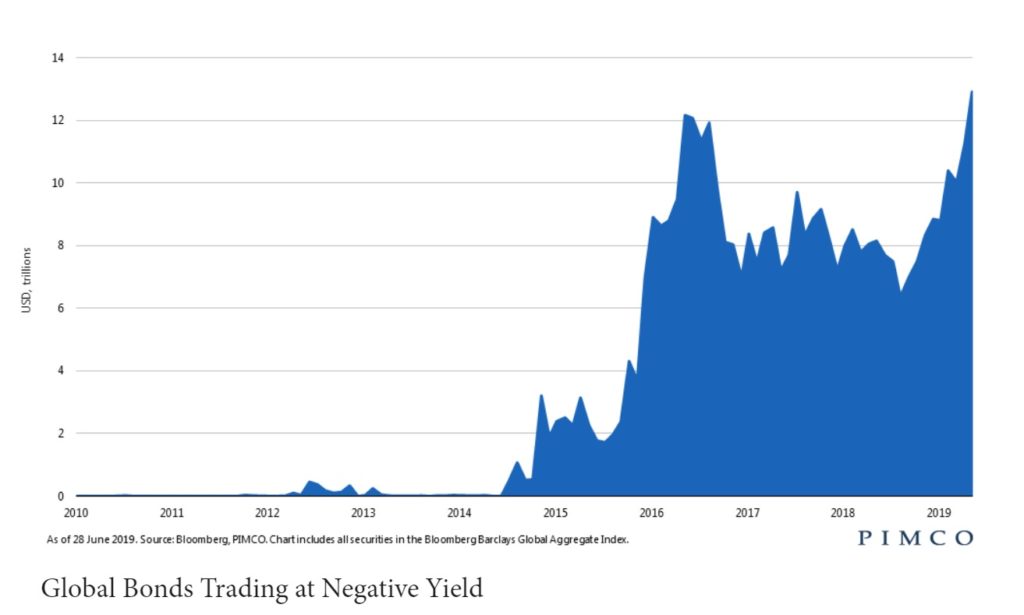

a) bond yields dropped to record lows (resp. below zero), so that more than USD 13 TLN of notional amount representing 1/3 of global Investment-grade rated Bonds carry negative rates in 2019. 4 This may have impact on Banks and Financial institutions future profitability, as they are forced to pitch for higher tickets and to go for bigger volumes in order to offset falling interest income. Based on that, their Balance sheets have become more exposed and more sensitive to the credit deterioration leading to a higher needs for potential loss provisions. And further, the Corporates sometimes tap the capital markets to raise the funds via issued Bonds, when they prefer not to be bound with any financial covenants (which is the case of loan agreements) and when they do not wish to provide any collateral.

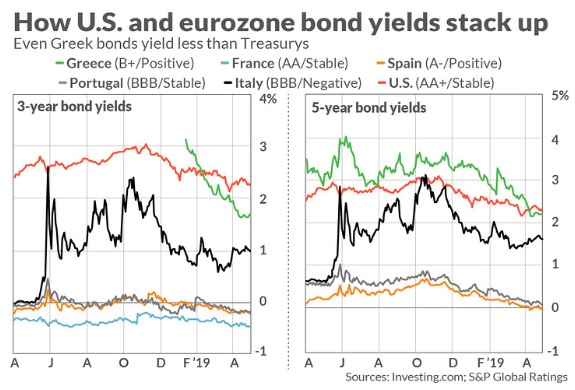

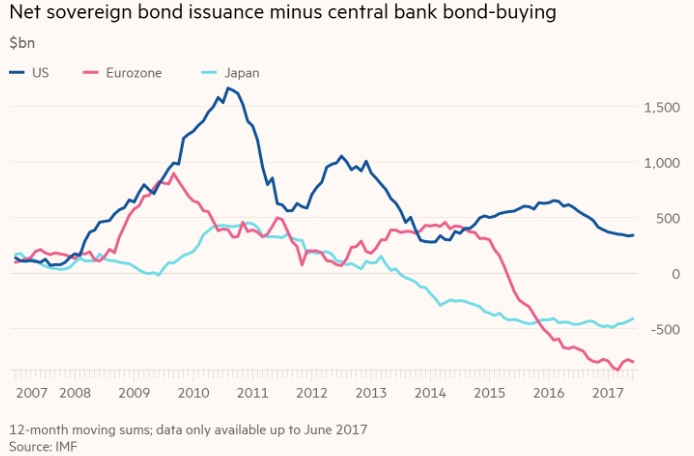

b) the yield spreads between core eurozone and the riskier countries were narrowed down, so that even Spain or Italy have been able to finance their public budget deficits at very low costs on Bond markets; for more details, please refer to below attached diagram. Regarding the topic on Yield spreads and their inversion, please visit the separate article, which can be found also here.

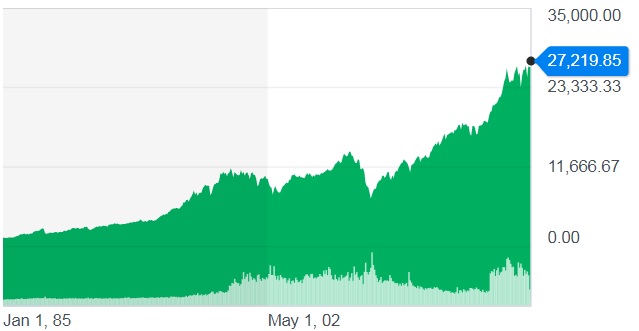

c) less expensive funding possibilities for Corporates as well as for Consumers have driven up the Capital market indices to their historical high levels (see below historical chart for Dow Jones index since 1985), so that ECB and FED find themselves in dead-end road, whereas they will most likely keep those stimulus in place not to invoke another market crash, which could potentially hurt global economy (“the more you fall from the peak, the more it hurts…”).

In general, respecting the macro-economic rules, each capital has its own price, and if this is not adequate to its costs, then the low price of the capital is demotivating for any financial savings.

Also, the Banks profitability might be negatively affected (the Banks need to earn sufficient level of interests from provided loans to cover the potential losses from non-performing assets) and higher market liquidity may lead to speculation purchase of assets like real-estates, which can further accelerate the inflation and price growth.

The very similar QE programmes were conducted in recent history by FED, Bank of England and Bank of Japan, however with relatively different outcomes. These outcomes may be relativelly connected with previously mentioned macro-economic aspects, which are different per each country. For instance, Japan keeps negative rates for more than decades, but still faces sluggish economy growth as it probably does not provide enough stimulus to boost the consumer spending. And this has perhaps origins in Japan life-culture as well as astronomically high prices for assets like Real-estates, so that even a rates close to zero do not help to convince consumers to purchase them.

However, the American way of QE conducted by FED in period 2008-2013 seems to have provided positive results, which also turns our attention to the question if those QE programmes were conducted in same way with same results. For instance, recent statistics actually revelead following:

- on US capital market, FED policy made interest rates lowered, so that Bonds issuances have notably picked-up during the QE period meaning that Issuers were able to place their Bonds for cheaper borrowing costs on public market among the institutional investors thanks to the available liquidity;

- on European capital market, the main buyer of a new Bonds still remained ECB as other market players rather prefered to place their liquidity with ECB, so that ECB has played a role of capital re-distribution manager.

ECB recently terminated its QE programme, but when making decision which way to continue, it has to take into account not only current conditions of domestic market, but also the conditions of largest foreign markets like US and Japan, which are most important competitors in terms of currency and foreign trade business.

So far, it is hard to make full assessment whether QE programmes had positive or negative effects on European markets, nevertheless certain hints may be provided by preliminary analysis prepared by Denmarks Bank senior economist. 1 Basically, as their main conclusions are following:

- positive effect on LT-stability of exchange rates

- no obvious bubbles on various assets markets /*

- Financial sector profitability remained healthy /*

- Corporate segment was also benefitting from zero rates

- Inflation expactations were anchored for a longer period

- negative interest rates combined with asset purchases and forward guidance appear to have been effective at all.

* these two statements may however appear quite bold as starting from July 2019, some Danish Banks (Nordea Bank and Jyske Bank A/S) started to sell Mortgage loans to its customers at zero rates (20 Years tenor) or even with negative rate of -0,5% (10 Years tenor). 2Such conditions usually lead to higher demand for housing units and their steep price growth. While negative rates with LT-lending products contribute to eroding the Banks profits.

Full text of this report is herewith attached:

For the past eight years of Mario Draghi presidency in ECB, he has shown an impressive determination to act. And, nothing is worse than a central bank admitting it has run out of the options.

In this regards, besides a possible rate cut, restarting QE looks as though it’ll be the most likely option. And as it has been officially confirmed, ECB will fully use available liquidity stemming from maturing Bonds that it holds in its Portfolio purchased under APP programmes, so that it may start to target Corporate bonds, as looking at the availability of assets, headroom in other purchasing programmes will be rather limited.

In addition, when speaking about Corporates, the Banks are also meant within this Subgroup of issuers. Basically, there are only minor criteria for such investments:

- ECB may buy up to 70% of issued volume of each Bonds issuance (ISIN) and the remaining tenor must be over 1 year;

- such Bonds must be eligible for collateral trading within Re-purchase transactions (so preferrably bearing Investment grade rating in case of Corporates and/or Senior-debt Bonds issued by Banks).

According to ING Bank economists, currently an EUR 700 bln eligible non-financial corporate euro investment grade universe is available on European markets. And that’s supplemented by an estimated gross supply of new eligible corporate bonds of EUR 150bn every year. And for the Senior Bank debts, a new eligible asset class worth EUR 305 bln is waiting for the ECB to be newly targeted. In the end, a total amount up to EUR 1 trillion could be purchased into the ECB Portfolio, each year.

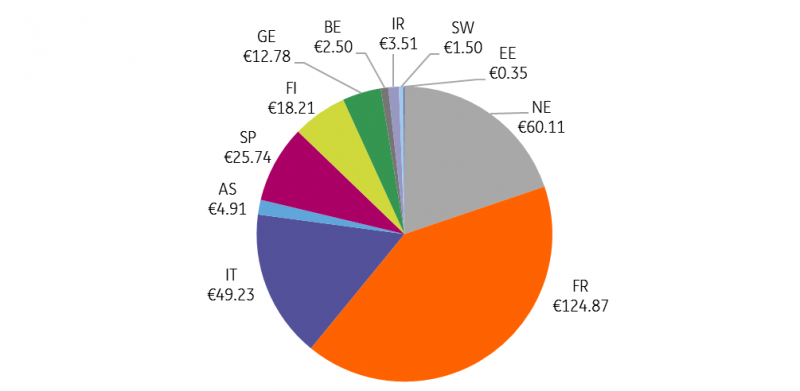

Looking at the charts, it seems that most of the bank debts would be issued by French, Italian and Dutch banks that will benefit most from lower funding costs as 40%, 16% and 20% of total debt eligible for purchase comes from these countries (see below attached chart with distribution per country in EUR bln amounts). 3

So, what implications may be expected, when ECB joins already over-crowded Bond market and starts purchasing these assets? Even it is hard to assess right now, it is quite sound to expect following results:

- Credit spreads resp. Yields will be squeezed, while Bond Prices will be rising, as current demand is already high given the low opportunities to reach reasonable return from investment; on other hand the Banks will benefit from lowered borrowing costs.

- Credit default swaps will be most likely reduced as well, nevertheless this will not be a result of improved credit standing of Issuers, itself, but of liquidity excess.

- Fund managers will have to change the investment strategy, as They will have to re-allocate the money into junk bonds in order to sustain the previous Yields, so that their Bonds Portfolio profile will become more risky.

sources: www.cnbc.com, www.think.ing.com, www.ecb.europa.com, www.imf.org, www.db.com, www.cnb.cz, www.ft.com

References: 1/ Morten Spange – „Low natural real interest rates and implications for monetary policy“, dated May 2019 2/ Emmie Martin – „Danish bank offers mortgages with negative 0.5% interest rates—here’s why that’s not necessarily a good thing“, dated August 2019 3/ Jeroen van den Broek, Carsten Brzeski: “Emperor Draghi’s not naked, the ECB has corporates (and banks) in CSPP2, dated July 2019 4/ Al Lewis – „How bonds with negative yields work and why this growing phenomenon is so bad for the economy“, dated Jul 2019