Next to the ISDA Master Agreement, there can be concluded also a Credit Support Annex (“CSA”), which is a legal document regulating eligible collateral for derivative transactions. It is an essential part of business relations in Derivatives and FX trading, but is not mandatory one. In other words, depending on the risk profile of both counterparties (assessed via their rating etc.), it is possible to deal purely based on ISDA agreement with or without an CSA. Annex means an attachment to original agreement, so that it is not possible to conclude an CSA without underlying ISDA Master Agreement (or its local equivalent).

Essentially, a CSA defines the terms and rules, under which collateral is posted or transferred between both counterparties to mitigate the credit risk arising from “in the money” derivative positions. Given this, there is a simple possibility to divide eligible collateral in 2 parts:

- Cash collateral (may be used for all Derivatives transactions)

- Securities pledged (only in case of Repurchase operations)

Depending on what kind of collateral is covered by CSA, the following terms are important:

- Initial amount, Transfer amount, Margin Threshold, Payment netting

- Haircuts resp. Valuation of collateral in form of securities

Speaking about Margining within Derivatives, this means that both counterparties agree on certain limits, up to which they are ready to tolerate the losses stemming from Mark-to-Market revaluation of concluded Derivatives. These limits may be bilateral or even unilateral. Further, Initial amount or Deposit to be placed upfront and Minimum transfer amount must be specified to have clear rules on margining. For instance if the following parameters were agreed:

a) Initial amount is EUR 500tsd.

b) Minimum transfer amount is EUR 100tsd. (and following multiplier of EUR 25tsd.)

c) Margin Threshold is EUR 50tsd.* (only with respect to counterparty Deutsche)

d) Margining interval may be Daily/weekly/Monthly or Quarterly

*/ based on EMIR update in 2017, the Margin threshold has been reduced to zero for all Derivatives, for details click here

Then, if Citi and Deutsche concluded any Derivative transaction, based on which Deutsche will face after 1 Month negative position (loss) of EUR 30tsd., then no action is triggered. However, if the loss deepens in following month, and it will be reaching EUR 60tsd., still the Initial deposit remains intact, as the minimum transfer amount was set to be EUR 100tsd., however Deutsche should start to be more worrying of losing money before the deal matures. Only if the cumulative loss reaches for instance EUR 130 tsd., then the amount rounded to EUR 125tsd. under collateral management will be transferred from Initial deposit, placed with some Bank or independent institution, from Deutsche to Citi. Afterwards, Deutsche needs to fund missing amount under the Initial deposit to original amount of EUR 500tsd. However, if this threshold was concluded only towards Deutsche Bank, and situation will change so that Citi will be facing losses, nothing actually happens and Deutsche have to wait until the maturity of the deal to receive its money back.

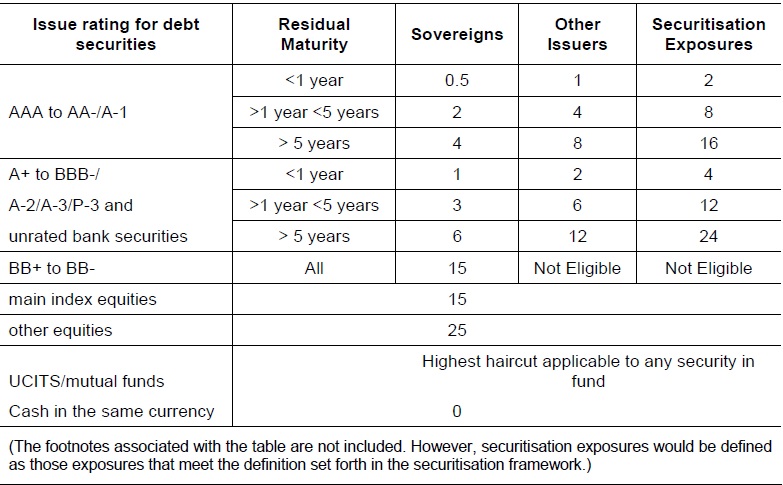

As concerns Repurchase operations, these represent quite specific transaction among Derivatives and there is actually no overlapping area with other related products (unlike Derivatives like IRS, Cross-currency swap, FX Swaps etc.). Repurchase operations represents regular loan which is secured with eligible Securities like Government Bonds etc. This kind of Collateral must meet the Eligibility criteria stipulated in CSA as well, e.g., currencies denomination, types of Bonds, their max. tenor and which haircuts are applied. For instance, 10% Haircut means that, when Deutsche Bank delivers Bonds in market value of EUR 100Mio, Citi will grant a loan of only EUR 90Mio. Having said that, these haircuts represent certain buffer for counterparty delivering the loan, for case that market value of purchased Securities would decrease during the deal life-time, so that the provided loan remains sufficiently covered (by 100%).

These haircuts are further derived from quality of Securities, which are reflected in the Issuer rating and tenor, actually. So that, an AAA rated 1Y Government bond will have an haircut of only 0.5% while the same paper maturing in 10Y will result to 4% of haircut. This must be specified in exact ranges for each Issuers securities in enclosed sheets, as a part of Annex A to CSA. For detailed haircuts, see attached picture depicting recommended ratios by BASEL Committee.

To distinguish between the Schedule to the Master Agreement and the Credit Support Annex, the schedules are numbered as Parts and CSA are numbered as Paragraphs. To customize the requirements of an OTC Transaction, the clauses which are required are added as Paragraph 11 (for London Agreements) and as Paragraph 13 (for New York Agreements).

Under English Law, CSA are considered transactions: Any collateral listed as ‘Eligible Collateral’ is delivered as an outright transfer of title. The collateral taker becomes the outright owner of that collateral free of any third party interest.

Compare the “Outright transfer” offered under English Law Credit Support Annex with “Security Interest” under New York Law Credit Support Annex. Both New York Law Credit Support Annex and an English law Credit Support Annex operate to create security interests in the collateral being posted, the differences are operational and can be material upon an insolvency of the other party.

- English law credit support annex operates by way of outright transfers of title to the posted collateral;

- Parties might select New York or English CSA for many operational considerations, also the choice of credit support documentation can materially change the parties’ rights and obligations and their standing upon an insolvency of the other party.