The European Market Infrastructure Regulation (EMIR) is Europe’s response to the G20 commitment to regulate over-the-counter (OTC) derivatives markets in the aftermath of the financial crisis. Corresponding measures in the United States are set forth in the Dodd Frank Act (Title VII).

In Europe, the execution of OTC derivatives is regulated under the Markets in Financial Instruments Directive (MIFID), whereas EMIR settles the issues relating to central clearing, bilateral margining and reporting.

EMIR aims to:

- Reduce systemic risk and increase transparency in the OTC markets

- Impose central clearing for standardised, sufficiently liquid OTC derivatives, mandatory bilateral margining for certain non-centrally cleared OTC derivatives and reporting to Trade Repositories (TRs) of all derivative trades

- Regulate central clearing counterparties (CCPs) and trade repositories (TRs)

- Allow interoperability among CCPs for equity and bond clearing.

In May 2017, the EU Commission published its EMIR review proposal. It aims to improve the functioning of the derivatives market in the EU and provide simpler and more proportionate rules for OTC derivatives. In June 2017, the EU Commission issued the second part of the EMIR review, concerning CCP supervision in the EU and third-country CCPs seeking access to the EU.

EMIR has had a profound impact on the way financial and non-financial participants operate their OTC derivative contracts.

Industry Implications

The scope of the transactions, which are taken into account in the threshold calculation, is somehow coherent across the main jurisdictions in Europe, Asia Pacific and the US. For example, physically settled forex forwards and swaps are now excluded across all jurisdictions. However, some countries (such as Hong Kong for equity options) may have temporary exemptions.

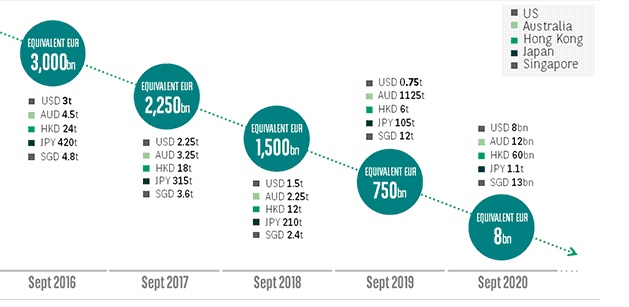

At the end of 2017, in practice, the counterparties with an amount of non-cleared derivatives above EUR 2,250 billion were impacted by updated regulation. Currently, as shown below, the threshold dropping world-wide from EUR 2,250bn to only EUR 8bn in September 2020, many more financial institutions including sell-side and buy-side, will be affected by this regulation. That means that, they will have to pledge a significant amount of collateral in order to cover the regulatory requirement. In addition, they will have to implement a specific framework to be compliant with the new rules.

Market participants have to comply with the new requirements as summarized below, which have an impact into mutual stipulations/ agreements concluded previously in MTA resp. CSA Annex:

- On all over-the-counter derivatives from 1 March 2017 with some special exemptions

- Daily variation margin (VM) to be exchanged between entities (excluding NFC- or Non-Financial Counterparties below the clearing threshold)

- Delayed application until 2018 for physically settled forex forwards

- Three-year temporary exemption for equity options (single stock and index) and lastly,

- Zero threshold to be applied

Treatment of collateral as defined by the new rules:

- Minimum transfer amount (MTA) which should not be higher than EUR 500,000

- Collateral to be “provided” on same day as the margin call, when no IM is exchanged between counterparties

- 8% cross-currency haircut to be applied to non-cash variation margin and to initial margin (cash and non-cash)

- Daily and two-way (bilateral) margining processes.

Other implications in practice:

Further, EMIR classifies derivative users into two types of counterparties: Financial Counterparties (FCs) and Non-Financial Counterparties (NFCs).

· Financial Counterparties: These include authorised commercial Banks and investment firms, insurance companies, registered funds, pension funds and private funds established in the EU.

· Non-Financial Counterparties: Any other undertakings established in the EU other than Central Counterparties (CCPs).

Direct compliance with the Risk mitigation techniques and the Reporting obligation of EMIR is required for all EEA FCs and NFCs. Compliance with the Clearing obligation and the Bilateral margining obligation is required for all OTC derivative transactions between EU based Financial Counterparties (FC) and EU Non-Financial Counterparties above clearing threshold (NFC+) at legal entity level, including non-EU based branches. Failure to comply may cause potential financial penalty and reputation damage.

The Clearing obligation also applies where one of the parties is a EU FC or NFC+ and the other party is non-EU entity (3rd country entity) which would have been subject to the clearing obligation had it been established in the EU.

Each EU-based Bank is classified as a FC. In addition to their own EMIR compliance, all EU based entities including non-EU based branches will need to fulfill the following obligation when concluding OTC bilateral derivative transactions:

- Transactions must only be with EMIR compliant counterparties and reported to Trade Repositories. A counterparty is deemed as EMIR compliant where it has a valid LEI, a valid EMIR classification and a signed EMIR terms with the respective Banking entity or Branch who is on the other side of the trade.

- Transactions within certain classes of OTC derivatives (as defined by ESMA) between FC and NFC+ (unless both entities are non-EU based) will be subject to mandatorily clearing.

- Non-Cleared transactions between FC and NFC+ will subject for bilateral margining (both variation margining and initial margining). Relevant legal documents (CSA’s) with strict Parameters incl. Zero Threshold and max. MTA of 500 tsd. EUR as stated above, need to be established before bilateral transactions can be executed.

Key dates:

- August 2012 – EMIR legislative process is finalised and the regulation enters into force

- March 2013 – Start date for effective implementation with risk mitigation techniques for non-centrally cleared OTC

- May 2017 – European Commission proposal for EMIR REFIT

- June 2017 – Second European Commission proposal for EMIR review – CCP Supervision package

- during 2017 to 2019 – Phased-in implementation of margin requirements for non-centrally cleared OTC derivatives

- in 2019 – Expected entry into force of the revised EMIR

source: www.BNPParibas.com