Options are described in general as Contracts that confer the right, but not obligation to buy (Call Option) or to sell (Put Option) some financial assets at a given price (called Strike/Exercise Price) on or before an specific date. The costs for having this right is called a Premium, which is the price that Buyer of Options pays and Seller of Options receives for receiving/ granting this protection. Options are de-facto considered as price insurance. The lower the odds of an option moving to the strike price, the less expensive on an absolute basis and the higher the odds of an option moving to the strike price, the more expensive these derivative instruments become.

This is pretty much different from other Derivatives, as this instrument provides hedging against future market changes, nevertheless the Owner of Options may decide, whether this right to buy/sell is exercised, based on current market prices. In other words, FX Option is like an FX FWD contract but with optionality to cancel the contract if current Spot-price at maturity of the deal is more favorable then what was pre-agreed under the FWD/Strike price. What is quite clear from this description, these Options are very beneficial to trade not only for FX-conversions, but also for Securities on Stock market. This is given the fact, that Stock prices historically show highest volatility among other trading assets, so that for Investors and/or Speculators, the best way how to secure the future right to buy/sell the Stocks at more favorable price, is to hold an Option to realize the transaction at best possible price.

The same principle is also valid for FX trades, whereas the holder of Call Option on EUR (traded as EUR Call/CZK Put or CZK Put/EUR Call) will have right to buy EUR-funds for selling CZK-countervalue in a future period based on pre-agreed Strike price, but considering actual FX-Spot for EUR/CZK. In order to decide whether this difference between Strike price and Spot price means reasonable profit, the costs of Premium must be taken into account. The understanding and valuation of Premium for Options was major task for two world-wide known economists Fischer Black and Myron Scholes, and they were first to publish a paper expanding the mathematical understanding of the options pricing model, and coined the term “Black–Scholes options pricing model. Later, in 1997 this formula received Nobel Memorial Prize in Economic Sciences. The key idea behind the model is to hedge the option by buying and selling the underlying asset in just the right way and, as a consequence, to eliminate risk. This type of hedging is called “continuously revised delta hedging” and is the basis of more complicated hedging strategies such as those engaged in by investment banks and hedge funds.

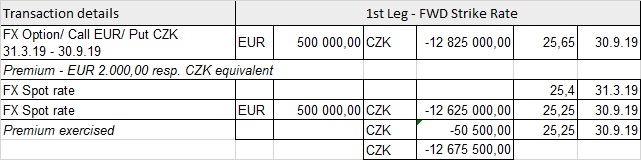

Example of an FX-Option:

In this specific example, IKEA agreed with Deutsche FX Option to hedge itself against weakening CZK currency, as it will need to pay EUR 500tsd. to various suppliers for delivery of new furniture and equipment into newly built Shopping mall. The completion of construction is expected to be at the end of Sept 2019, but it can be delayed in reality. So therefore, instead of concluding an FX-FWD deal, it has decided to buy an Call Option on EUR in case that EUR will rise during this period. Current FX-Spot EUR/CZK rate is 25,40 while there is expectation on market that it will further rise during the Summer, so that Deutsche offered an Strike rate of 25,65 with Premium of EUR 2tsd. In reality, Czech National Bank has changed its policy and increased interest rates on CZK-funds, which led to minor correction of CZK rate vs. EUR upwards (FX-Spot is 25,25 currently). As the Option is nearing to the expiry date (30.9.19), IKEA will have to consider either to:

1) simply exercise the Option and buy EUR funds for CZK 12,825Mio as pre-agreed at Strike price (25,65 EUR/CZK) incl. the Premium costs or

2) not utilize the Call Option, but to pay to Deutsche only Premium price (in equivalent of CZK 50,5tsd.) and to purchase EUR on FX-spot market so that total costs equal to CZK 12,675Mio.

Quite clearly, second alternative is better for IKEA as it will save quite interesting amount of CZK funds (12,825Mio – 12,675Mio), which is possible only under FX-Option transaction to decide based on current market prices and choose proper alternative.

In general, Corporations primarily use FX options to hedge future cash flows in a foreign currency. The most usual rule is to hedge certain foreign currency cash flows with FX-forwards, and uncertain foreign cash flows with FX-options.

Due to very high liquidity on the Options market, each market participant may de-facto buy and sell the Call/Put Options based on their expectations, how would market develop in the future and depending on the situation whether they already keep the underlying assets to be hedged or just intend to purchase/sell these assets. Reflecting this, there are basically four Options transactions possible to be dealt:

- To buy (Long) Call Option (right to purchase) => when You expect the bond price will rise, but you do not own the Bond so that you will be able to buy it below the market price.

- To buy (Long) Put Option (right to sell) => when You expect the bond price may fall and you already own the Bonds, so that you will be able to sell it above the market price.

- To sell (Short) Call Option (right to purchase) => You expect the bond price will fall or remain static, but you do not own the Bond yet and you do not have the motivation to buy it.

- To sell (Short) Put Option (right to sell) => You expect the bond price will rise or remain static and you already own the Bond, so there is no need to hold this protection.

In addition, there are number of variations on Options like for instance, Caps and floors, which are options on market interest rates (e.g. Libor) to secure the minimum or maximum floating rate to be paid/received. Further, there are traded also Swaptions, which are in fact options on long term interest rates, (IR-swaps), also Barrier-options etc. As seen from above, this Product is quite complex and provides large optionality, so that it is hard to describe all alternatives and possibilities for what kind of trading strategies it could be used.