Cross-Currency swap (XCS) can be described as combination of FX-swap and IRS, as the counterparties conclude on swapping two currencies at beginning while this is accompanied also with connected interest flows. The only exception for this analogy is that there is switch between interests flows based on market rates (e.g. PRIBOR vs. EURIBOR), and not for fixed rate as in case of IRS. Similarly as in case of an IRS, the notional amounts are swapped back to original currency just at maturity of the deal, however calculating via FX FWD rate (instead of FX-Spot).

What is apparent from this description, this Derivative is quite a complex transaction and from risk point of view, the real market-value in time of this transaction is derived from (a) mutual development of FX-rates and (b) interest rates movement. XCS transactions are attractive for international investors, who hold vast portfolio of LT-assets denominated in various currencies and seek for options how to reach better Yields from alternative denomination of those assets. This type of transactions are very useful also for “Speculators” who predict certain development on interest rates in the future and make bets on their increase in the future. For a market quotation of Cross Currency swaps, there are “Swap basis points” taken into account, which effect FX-FWD rate for conversion of notional amounts at maturity. This element should basically reflect the “interest differential” which enables different options for generating different Yields from various Currencies placement. Historically, e.g. EUR/USD Basis swap points development has also indicated resp. reflected global situations (for instance, widening of Basis swap points occured when EU markets were distressed, while flattening of these swap points took place in opposite situations, e.g. continuation in Quantitative Easoning conducted by ECB, consolidation of EU financial stability etc.). See below attached Diagram showing development of those points in most recent period.

Currency swaps have following reasons for trading:

- To secure cheaper costs for debt funding (by borrowing at the best available market rate comparing between PRIBOR, EURIBOR, LIBOR etc. regardless of underlying Debt denomination and then swapping for debt in desired currency using a back-to-back-loan) or alternatively,

- To reach higher Yields from holding LT-assets while the assets in another currency (deposits, purchased Bonds etc.) bear higher market rates.

- To hedge against FRA market rates changes.

- To defend against financial turmoil by allowing government authorities (like Central Banks) to borrow money on better terms with its own currency.

For the reasons of (1-2) the motivation is almost identical, with only difference that Counterparties search for lower costs or higher revenues from holding LT-liabilities or Assets. In particular cases, we are very often witnessing on the market following actions:

Ad 1) IKEA CR is a domestic retailer, so that its income is mainly in CZK, while on the contrary the costs structure is for instance CZK (60%)/EUR (40%). As it is borrowing LT-loans on CR market for PRIBOR + relevant margin, however current EURIBOR rates are lower and close to zero, it may be beneficial for IKEA based on concluded XCS with Deutsche, to have swapped CZK into EUR funds and to pay lower rates for these funds. Nevertheless, this Interest Rate-related benefit may be off-set with FX-FWD conversion done at deal maturity, which may bring some additional costs.

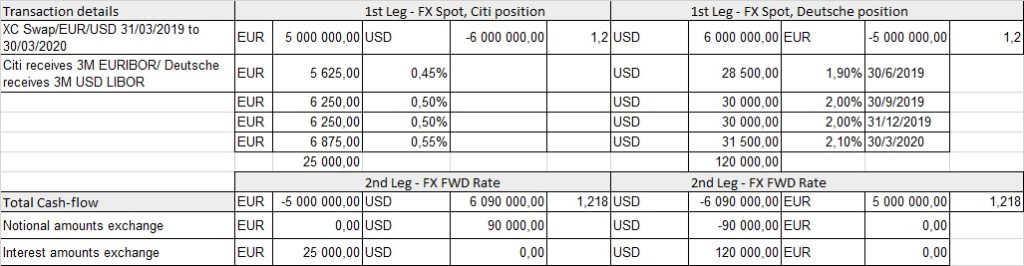

Ad 2) European-based Investment/Pension Funds/Banks adn other financial entities have large positions in EUR on both sides, i.e. Clients deposits as well as Investment assets, but seek for better revenues, as current EURIBOR rates generate almost negative Yields. So that, Investment Funds may decide to swap EUR deposits into USD deposits and purchase US T-Bills with attractive Yields or simply place USD-deposits on Money market, but still for substantially higher revenues than on German Government EURO-bonds, which are linked to EURIBOR. For detailed calculation, see below attached example.

In this particular case, Deutsche sells EUR-funds to Citi and receives USD at FX-spot rate (1,20) and then benefits from higher USD-linked interests. However, at the end of deal, Deutsche buys EUR back from Citi based on pre-agreed FWD rate of 1,218 so that it has to deliver more USD then originally bought from Citi, which is compensating the interest-differential.

Ad 3) whereas the Counterparty may be exposed to future rise of FRA-rates which define future values of market interest rates like LIBOR, EURIBOR etc., this risk may be mitigated also via XCS, whereas the Funds are swapped into another currency with lower interest rate. This is in fact very similar alternative to Case (1), whereas IKEA CR has already CZK-denominated borrowings in place and is afraid of future development of PRIBOR rate as its Debts are linked to this floating rate, so that it can convert these funds to EUR and hedge against the PRIBOR risk (however to remain exposed to EURIBOR risk, which is though expected to remain flat, so that this risk is more predictable).

Ad 4) there have been in the past established Stand-by bail-out facilities to deliver market liquidity in financial turmoil conditions like US Fed did in 2008, resp. Republic Bank of China provides Renminbi support to Asian-based central Banks and/or on certain bilateral individual basis. For example, “Goldman Sachs helped Greece to raise $1 billion of off- balance-sheet funding in 2002 through a currency swap, allowing the government to reduce the national debt costs.” Greece had previously succeeded in getting clearance to join the euro on 1 January 2001, in time for the physical launch in 2002, by virtually reducing its deficit figures (when compared with GDP).