Interest rate swap (IRS) represents core Derivative deal aimed at hedging against Interest rate risk. It is quite simple arrangement between two Counterparties, about swapping the basis for Interests calculation on any Loan, Corporate Debt, Debt paper or another instrument bearing floating interest rate. Basically there may be following motivations to conclude an IRS deal:

a) Hedging against future rise of market rates, so that entity buying this protection will have secured fixed rate for entire period of the underlying instrument life-time. This is mostly the case of LT-loans, when Clients prefer pricing which is lowest at moment (like 1M PRIBOR, 3M EURIBOR etc.), however after the loan is drawn, there may arise some indications of changing policy adopted by Central Banks, which will shift also interest rates upwards in near future.

b) To achieve Commercial cross-sells when the Bank tries to increase the commercial income generated from relationship with Client and next to the provided loan, which has a floating pricing, there is possibility to conclude IRS and thus placing also Financial markets products with Client.

From risk point of view, IRS bears quite low risk weights as there is only exchange of interest flows, while Principal amounts are not exchanged between Counterparties. Therefore, also Settlement limit is not utilized, at all.

Below attached example shows the transaction calculated on principal amount of CZK 10Mio, whereas IKEA had a loan from Deutsche with floating rate of 3M PRIBOR for a period of 1Y. In order to protect itself against movement of market rates (increase is forecasted), IKEA concluded an IRS with Citi for same transaction.

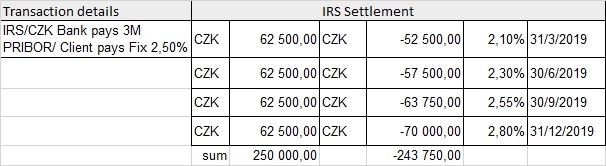

As a result, following flows will be realized:

- Citi has agreed to pay to IKEA floating interest based on current 3M PRIBOR (changing in time from current level of 2,10% p.a. up to 2,80% p.a.).

- IKEA will be paying de-facto the same interests from the loan with Deutsche, so that these flows will be zero-effective.

- Citi will be receiving from IKEA fixed interest rate of 2,50% p.a. each quarter.

What is apparent from this overview, total difference in cash flows is quite low (CZK 250tsd. – 243,75tsd), which represent costs of hedging for IKEA, which is well acceptable compared with loan amount of CZK 10Mio. Secondly, this also means that IRS deal was fairly priced by Citi, so that Client was not over-paying the Bank, so much.

In reality, the IRS should de-facto reflect any expectation for future market rates, so that the Fixed rate paid within IRS should be an average of those future rates. This is also shown in the calculation, that first two Quarters, the Fixed rate (2,50% p.a.) was still above the PRIBOR, while during the last two Quarters the market went up to reach the rates equilibrium.

Another examples from practice:

As mentioned above, IRS can be used as hedging tool for any instrument bearing floating rate. So, that besides LT-loans, also Debt papers may serve as underlying transaction for that. And this need may arise on both sides in the same extent, so that Debtors as well as Creditors may seek this option. An Issuer of Bonds with floating coupon rate may be in same position as well as Investment/Pension Fund, which purchased the same Bond, may be eager to secure the fixed rate coupon, so that the interest costs/Yields will be known/fixed upfront.