A Tiering system (two tier system officially) for liquidity excess was introduced in Sept 2019 by ECB to provide the banks with certain relief in the Euro-zone area of negative rates (for a full press release by ECB, click here), which has negative implications on Banks profitability. Especially during the last five years, the european banks have stashed free reserves exceeding EUR 1,9 tln which then translate to additional costs in range of EUR 7,5-10 bln from deposits with ECB (representing almost 10% of total banking sector profit in 2017). In addition, especially in case of German banking sector, where the large banks suffer from operating losses, overal picture gets much worse, as they paid nearly EUR 2,5 bln out of total profit around EUR 12 bln just two years ago. (1)

And with re-started QE policy by ECB in 2019 respectivelly in 2020 based on forward guidance, there is no outlook for dramatic change, so that the Banks would be negatively hit again, if there was no exemption provided. And banks naturally cannot pass these extra costs on private depositors in full range.

EU banking system is typical for huge liquidity excess for a long time, meaning that banks face problems to find adequate opportunities for financing such projects (and clients), that would reward them with sufficient revenues in form of interest income while compensating undertaken risk. And this is crucial aspect for Banks profit and loss statement, as usually they place their liquidity excess with central banks. This is simply the only alternative for safe investments, whereas Government Bonds Yields also fell below zero and demand for interbank deposits has minimized as well given the liquidity excess.

First, it must be noted that tiering system is no experiment and it has been used also in some smaller countries like Denmark or Switzerland, but question is how this will work in larger „heterogeneus“ market like whole Euro-zone. In fact, some analysts have argued from the beginning that certain side-effects could be expected, e.g. Italian bond market might be affected due to lower liquidity of Italian banks, for instance. Another argumentation claimed that this will represent the monetary tightening in fact, as average rate on money-market is set to rise herewith (based on current exempted reserves it would result to -28BPS roughly).

So, how it works?

Well, it is quite simple. At moment, the banks have possibility to keep their cash excess either with local bank (on current account) or with ECB (in form of deposit). The placement of liquidity excess on current account is usually non-remunerated so that it brings zero interest income to banks (respectivelly the lower one between Deposit rate and zero rate). The deposits placements with ECB, have been priced in line with ECB monetary policy, as this deposit rate is one of the main three interest rates. Until July 2012, deposit facility rates had been positive, afterwards turned to negative one and have remained so, until now.

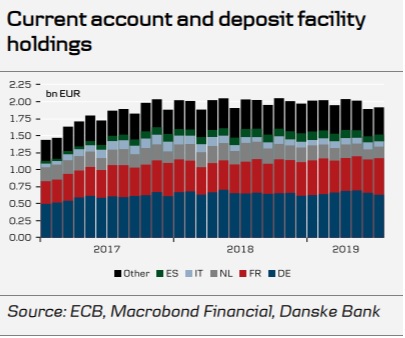

Tiering system has been designed based on current requirement for Banks minimum reserves, which stood at EUR 120 bln (or 1% of total Balance sheet with Euro-zone banking sector) in July 2019. For more details, please see attached chart:

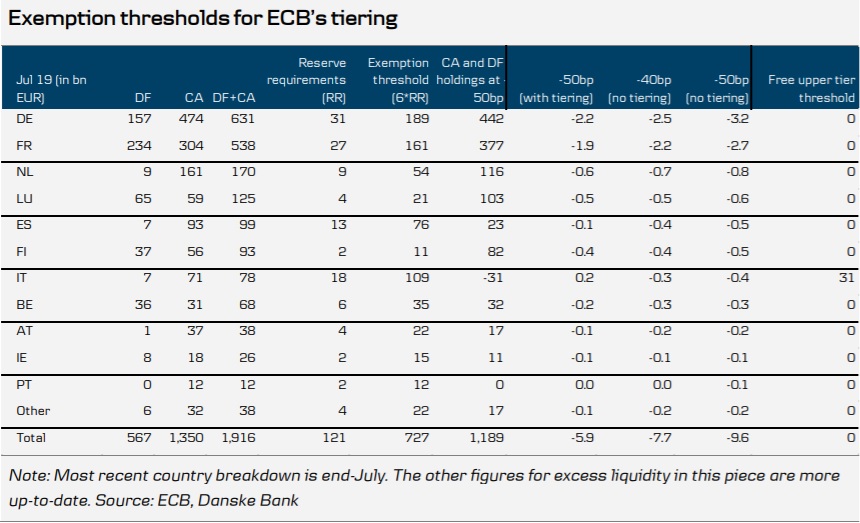

In line with that, ECB has set an threshold of 6,0x up to which the banks are now allowed to place their cash excess with ECB, while still benefit from so called „Upper tier“ rate, which is zero rate. This means that out of total cash excess roughly at EUR 1,9 tln there are „exempted“ reserves around EUR 730 bln, which will not be „punished“ with negative rate of 50 BPS. (2)

This two-tier system applies to excess of liquidity held in current accounts with the Eurosystem but will not apply to holdings at the ECB’s deposit facility. This will represent a substantial relief in costs for EU core-countries like Germany, France and Netherland, which hold the major part of free reserves within Euro-zone. For more details, please refer to below attached chart.

On the other hand, as already mentioned, Italian banks are de-facto „cash-short“ according to these new parameters meaning that they could place with ECB for free of any charge up to EUR 110 bln, however their cash excess balance stood at EUR 78 bln in July 2019. This means that Italian banks have been offered with a simple arbitrage opportunity, whereas they can simply borrow money on local Bond repo market (still at negative rate) and park these funds with ECB (at zero rate). Very first statistics indeed showed increased holdings of Italian banks with ECB current account by EUR 37 bln at the end of October 2019, while net interbank borrowings decreased by EUR 48 bln, at same time. (3) This might lead to increased profits by some EUR 200 Mio per annum, without undertaking any risk.

Conclusion

The question whether this was meant as special gift from former ECB Chairman Mario Draghi for Italian banks, when he was leaving the office, would be a pure speculation however. What is quite clear on the contrary, that this Tiering system leaves open doors for ECB for another potential rate-cut in the future, if needed, while possibly increasing the exemption threshold, so that the negative impact on the banks would be reduced herewith.(4)

In addition, ECB is not concerned with any side effects of Tiering system on individual market as they are deemed to be rather a marginal without any signifficant influence on functioning of whole inter-bank market. On the contrary, ECB is very satisfied with how the Tiering works so far as it gives protection against any risk to the credit transition channel.(5)

Sources:

www.ft.com, www.reuters.com, www.fxstreet.com, www.e-markets.nordea.com, www.omfif.org, www.ecb.europa.eu

Referencies:

1/ ECB Watch: Could tiering save bank profitability? By Jan von Gerich, published in March 2019

2/ ECB Research by Danske Bank, by P.H.Christiansen, published in September 2019

3/ Italian banks taking advantage of ECB tiering system, by William Coningsby-Brown, published in November 2019

4/ Italian banks rush to profit from ECB negative rates, by Martin Arnold, published in November 2019

5/ Reuters interview with Philip R. Lane, an ECB Executive Board member, published in September 2019