The initial version of MIFID, that came into force in 2007, was intended to be a corner-stone of EU efforts to create a single and harmonized financial market as it mainly sought to end the monopoly of US capital markets as well as to drive down the costs and connected risks for investors. However the following reviews undertaken by EU Commission in 2010, revealed main shortcoming that is was primarily focused on equities trading. Afterwards, before end of 2011 the EU regulators finalized the revised version of MIFID that was even more ambitious in order not only to cope with new technological standards but also to tackle the unregulated markets covering newly Bonds and other Derivatives trading. These updated rules were supposed to reach-out across the financial markets, from banks to institutional investors, hedge funds and brokers, stock exchanges and even high-frequency traders.1

When MIFID met EMIR, the “Big-Bang” was created

Since 2014, revised MIFID regulation together with the Markets in Financial Instruments Regulation (MiFIR) were formally adopted by EU insitutions, creating together the legal framework governing the requirements applicable to investment firms, trading venues, data reporting service providers and third-country firms providing investment services or activities in the EU. They are applicable from beginning of 2018 and together referred to as MiFID II.

While the initial edition of MIFID focused on client categorisation in order to reach their protection based on their market expertise and knowledge, the revised edition of MIFID added into it enhanced target to provide clients with improved transparency and full disclosure on the product appropriatness, costs for investment research, market price and other related best execution practices when trading with respective products. Additional aim of regulators was to push the investors away from phones to electronic venues, for better audit trails and surveilance purposes.

MIFID II structure

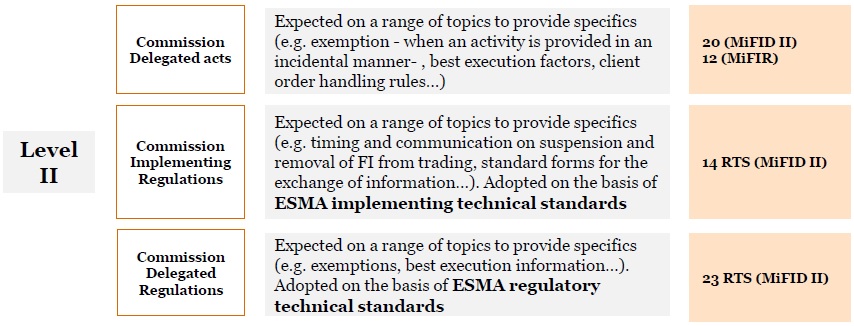

MiFID II aims at increasing investor protection by creating a more effective, efficient and transparent market for investment services and activities in the EU. Details of updated measures applicable to each Article of MiFID II are set out in following parts:

- EU Commission delegated acts,

- EU Commission implementing acts and

- EU Commission technical standards (drafted by European Securities and Market Authority – ESMA, the Pan-European regulator).

As further elaborated, the main areas governed by updated MIFID can be categorized as following:

1. Clients protection: Adequacy of financial products to be more tailored made to the customers knowledge and experience, so that these will be oferred on respective market and to proper category of the clients. That means, the scope of offered products under „Complex“ category is to be broadened, so that financial firms will be able to sell fewer products to investors without needs for assessing their literacy (Execution only principle). This is to be connected with higher transparency and disclosure on product structuring and related costs, so that it becomes more comparable with other. Improved product governance rules should also help to achieve targeting the proper market segment of customers.

2. Distribution: main target is to reduce the commission payments, as Investment managers and their distributors (advisors) are expected to become independent, so that their primary motivation of just raising the advisory fees for a questionnable investment will be muted. Advisors should not even receive some compensation fees for navigating clients towards the certain trading venues, otherwise their independent status could be disputed due to conflict of interests. MiFID II regulation herewith aims to provide better customers protection against unresponsible advisory activities. Based on this, Investment managers are likely to set-up a multiple distribution channels, which serve a specific client segments.

3. Markets and Trading venues: following the recent equities market fragmentation, some trading venues shifted to so called „dark-pools“. Therefore, to avoid similar trends in Bonds and Derivatives, the competition across the regulated and alternative markets to be more under control, so that market disruption risk is reduced with higher effectiveness of financial transactions. And thats why, the main goal is to reduce Derivatives traded purely on OTC market and to create OTF venue for trading with Bonds. Further, MIFID II regulation to be newly implemented and adopted on financial instruments, that were not covered by initial version (e.g. structured deposits). And lastly, the regulators should have newly the possibility to ban trading with certain financial instruments, which derail the stability of financial markets.

4. Investment research: Unbundling process means that Fund managers and Investment advisers will have to budget separatelly research and trading costs. This step was meant to cut the transferring of virtual costs for analysts reports and research onto the clients into the margins/spreads, which was seen by regulators as conflict of interests. This was due to estimated amount of EUR 33bln per annum that European Asset managers pay to their distributors as a fee, which in eyes of regulators, made the wealth management as an attractive industry, but not always serving to customers priorities. In fact, some research showed, that Investors having placed their savings into Funds, actually received less after deduction of fees, as if they just purchased main Stock Indexes.2 For details, see below:

5. Transaction reporting: a shift of T+1 reporting duties from Brokers onto the Trading companies (in-house reporting), plus increasing requirement for reporting of almost 65 parameters to each transaction (under MIFID I „only“ 23 were required) will be representing higher administration burden on Investment companies.3 And, each financial insitution is obliged to keep statistic data for period at least 5 years about these transactions.

6. Transparent calculations: Investment banking services to remain fully independent, which cast still some shadows on area of financial stimulus and incentives for investment companies. Due to the fact that initial version of MiFID was not going so much into details regarding this topic, MiFID II makes more emphasis on transparency of mutual relationships of all counterparties. Securities traders and investment firms, which wish to be categorized as independent, they should not charge fees or receive compensation money from third parties, as a result of purchasing financial products on behalf of client. So that, they are obliged to advise their clients, whether they act on independent basis or if they receive some premium for intermediary services. Further, financial advisers are required to execute the investment order (to sell or purchase) for best conditions with regard to execution price, costs, speed, size and other criteria. MiFID II further outlines also criteria, which defines best execution order.

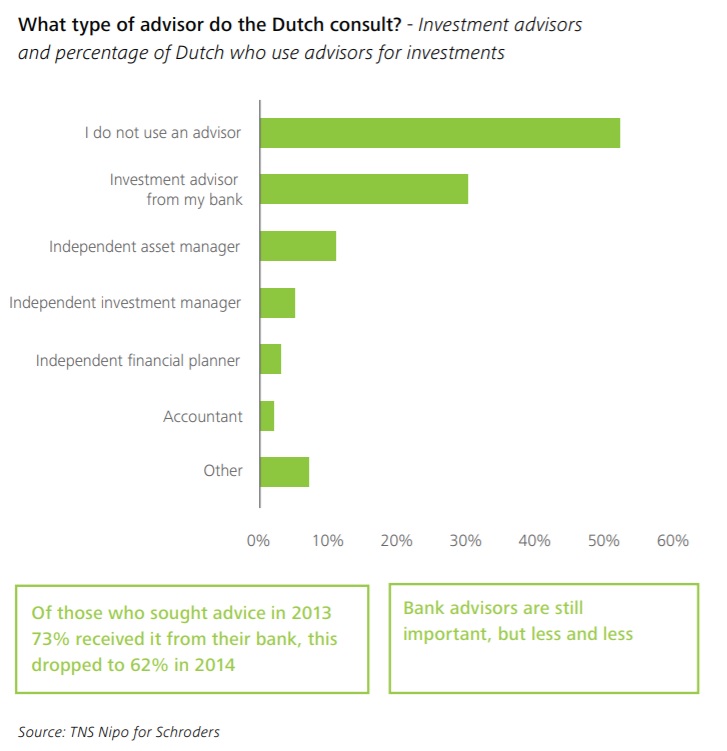

Below attached diagram shows the results of an research on, how typical Dutch investor use advisory services when investing:

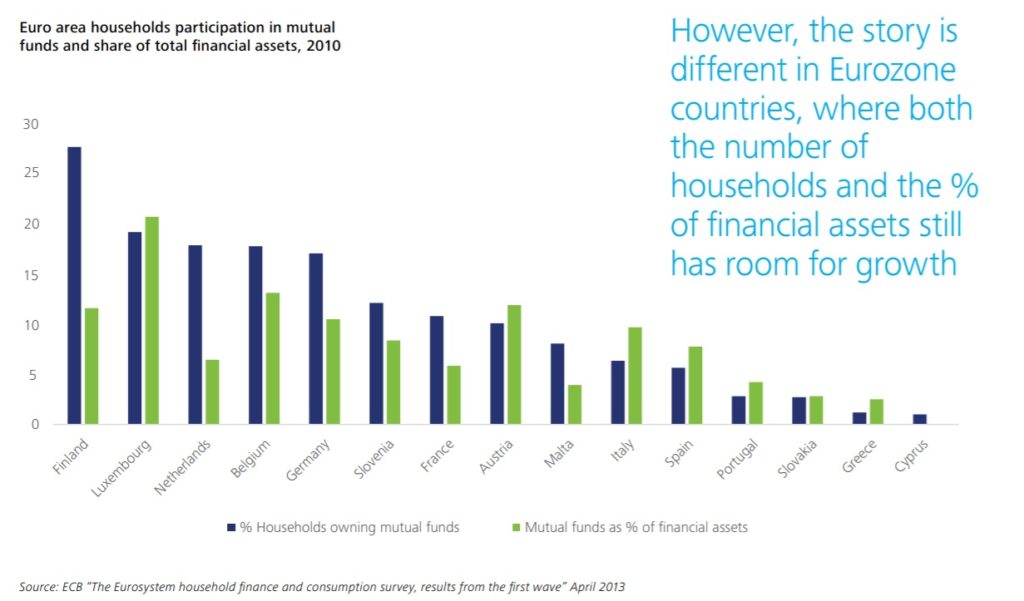

7. Operating model: as the working environment for Investment firms is getting more sophisticated and administrative/regulatory requirements are more complex, it raises some doubts whether EU-based institutions will be able to compete with other (like U.S. asset managers operating on-line via web), which still have straight-forward business model and do not need to comply with all the rulles imposed by European regulators. This may be connected with fact, that European households still keep their vast part of money with bank accounts (more than 40% of their assets), so that they still represent by far the most attractive clients in wealth management (for details see below attached charts).

8. Product intervention: since April 2019, ESMA agreed together with other European regulators on prohibiting the sale, marketing and distribution of CFDs contracts and Binary options to retail customers. This applies mainly to highly volatile deals, that include high leverage in uderlying assets (like 5:1 for Equities, or 10:1 with Derivatives and 30:1 with major currency pairs etc.). Such contracts simply bear inside increased risk that could lead to unexpected losses for a retail customers, which they can not recognize upfront. 4

As a short summary, in line with updated MIFID regulation, Investment and financial institutions need to properly set-up their distribution channels, advisory model, targeted clients segmentation and trade execution processing, which will altogether mean a big challenge for everyone in financial industry.

sources: www.deloitte.com, www.esma.europa.eu, www.nbs.sk, www.ft.com, www.pwc.com

References: 1/ Philip Stafford, Peter Smith: „Europe begins the countdown to MIFID II“, dated January 2018 2/ Deloitte WP: „MIFID II – What will be its impact on the investment fund distribution landscape?“ dated November 2015 3/ MIFID II, Transaction reporting: Detecting and investing potential market abuse, published by PwC, July 2017 4/ ESMA: „Provision on CFD and other speculative products for retail customers under MIFID“, published in March 2019