Factoring means purchase, funding, management and collection of short term accounts receivable arising from supply of goods and services to domestic buyers. Goods are delivered on open account credit terms up to 180 days. Basically, we recognize two categories:

a) Recourse factoring and

b) Non-recourse factoring.

Factoring market segment, or globally called Supply chain financing, is currently representing the very demanded service from Corporate customers, as they seak for (i) optimization of Cash-flow (ii) funding diversification (iii) transfer of risk – off balance sheet treatment (iv) flexibility and certain portfolio approach combined with operational excellence. Based on that, this type of service is deemed as solution that is very much complementary to usual Working capital financing. Global leaders are therefore seen in Citibank, HSBC, ING Group, Santander, Unicreditbank, Societe Generale, BNP Paribas etc.

Essentially, as a result of cheap funding available world-wide, after financial crises in 2008/09, many independent platforms (so called Fintechs) have risen to create strong competitors to traditional Banks. These entities are represented by PrimeRevenue, Kyriba, CRX Markets, Taulia, ORBIAN and many others. Apart from Factoring/ Receivables purchase, their core business is also represented by FX operations and Treasury management. These independent platforms offer good functionality and quick response to market development, however they have following weaknesses:

- they are rather an IT companies, so they need a third-party partner for settlement of payments, which is a Bank in the end (so they must cooperate with competitor)

- they are typical for longer and more rigid contract negotiations (any changes to the contract must be consulted also with a funding party); in addition they have very limited local presence and their documentation is governed by English or NY law, and nothing more

- Remuneration income is based on processing fee; except for FX transactions they do not aim for additional cross-sells as they do not follow LT strategy like a Banks do (this has potentially negative implication in general, as FinTechs are more likely to withdraw from market when their Business model is not profitable enough).

- On-boarding activities are typically carried-out by Call centers, which may be a bit anoying when compared with direct Relationship with the Bank.

However, in the end, these non-bank platform must be seen as challenging motivation factor for standard Banks or Factoring Companies, which are forced to further develop and improve their services, business platforms and approach as such.

Factoring Coy (Company) offers recourse factoring; it means that in case the account receivable is not paid in 90 days after the due date at the latest, it is reassigned back to the client. This is the cheapest way of financing, but ultimately the risk of non-payment remains in the books of Supplier. So, it can be considered as bridge financing to cover the short-term Cash shortage.

Non-recourse factoring with insurance is another alternative. The advantage of this option assumes that Factoring Coy arranges all negotiations with insurance company including applications for insurance limits and reports of insurance events. Insurance refers exclusively to cases of domestic buyer payment default and/or financial insolvency. In case of insurance event, the client will receive 85% of the account receivable value; 15% represents client’s participation on the risk.

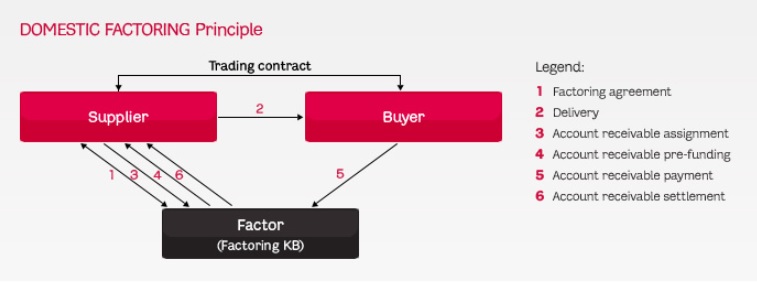

FACTORING Main Principles

- Factoring Coy concludes a domestic factoring agreement with the supplier.

- Supplier provides goods to the buyer including an invoice which contains assignment clause informing the buyer that the account receivable is assigned to Factoring Coy.

- Supplier assigns account receivable to Factoring Coy (supplier has the option of electronic account receivable assignment).

- Factoring Coy pays so-called advance to the supplier in an amount of 70–90% of the account receivable value.

- Buyer pays account receivable in full to Factoring Coy account.

- Based on the payment receipt, remaining account receivable of 10-30% is settled with the supplier after deduction of related costs/fees.

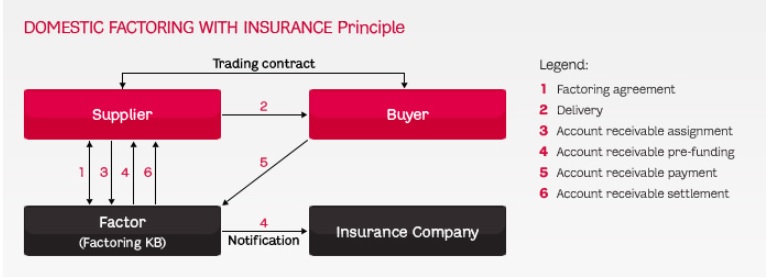

FACTORING WITH INSURANCE

For this type of an agreement conclusion, determining insurance limit for selected buyers is essential. The main advantage for Client (Supplier) is that there will be no recourse in case that Buyer will not pay for the delivery, on the other hand there must be certain credit history of this Buyer available to Insurance company.

- Factoring Coy concludes a factoring agreement for domestic factoring with insurance with the supplier. The factoring fee as a reward for managing the account receivables usually amounts to 0.3–1.0% of the account receivable notional value. On top of that, there are usually costs of funds associated with this product.

- Supplier provides goods to his buyer as a Factoring Company`s client.

- Supplier assigns account receivable (invoice with assignment clause) with the necessary documentation to the factor.

- Factor provides the client with funding for account receivable advanced payment based on contracted amount and reports the account receivable to the insurance company.

- Buyer pays the invoiced amount to the factor’s account within the pre-agreed deferred due date (usually up to 90days).

- Factor pays the remaining amount of the invoice reduced by agreed fees and interests to the supplier.

In case the account receivable is not paid in 90 days after the due date, the Factor reports an insurance event to the insurance company. Then, insurance company will check, whether all contractual conditions were met by Supplier, especially in terms of validity of running insurance contract, delivery of the Goods etc. After completing all checking mechanism, the Insurance company pays to the Account of Factoring company directly.

FACTORING and its Advantages

- increase of competitive advantage by providing goods through open account credit terms with maturity of up to 90 days (180 days in exceptional cases)

- possibility to draw funds immediately through overdraft option in the account receivable currency, usually 70–90% of the nominal value

- advanced payment usually provided within 48 hours from receiving account receivable documents

- goods sales volume extension through funding without the usual security required by the banks in Working-capital financing (like Promissory notes, Parent guarantee etc.)

- better planning for future cash flows and online communication allowing account receivable assignment and providing daily overview of accounts receivable, advances and incoming cash collection

- account receivable management takeover by the factor leading to operating cost decrease

Costs Associated with FACTORING

- Factoring fee: Includes cost connected with administration, collection or insurance of accounts receivable assigned to the factor Usually amounts to 0.3–1.0% of the account receivable value.

The price can be increased by premium in case of non-recourse factoring. - Interest costs: Interests are charged on advances provided for assigned accounts receivable based on short term bank credit rates.

- Insurance costs: depending on volume of insured receivables, default ratio and payment discipline of Buyers, etc.

- Audit fees: these may reach around EUR 10tsd., when audit is carried-out by a Big4 Audit company, or less if local company is engaged. Audit of the quality of Receivables becomes more frequent pre-requisite for these operations.

EXAMPLE

Invoiced amount: 100 000 CZK

Due date: 60 days

Factoring fee: 0.35%

Funding interest: 1M PRIBOR + 2.0% p.a. = 2,6% p.a.

Advance payment amount: 90%

1st day Supplier issues an invoice and sends it to a factoring company with a delivery note.

2nd day The factoring company calculates the advance payment amount and pays a supplier

100 000 x 90 % = 90 000,- CZK.

61st day The customer (Buyer) pays a factoring company 100 000 CZK for goods delivery. The factoring company pays the supplier 10 000 CZK and calculates the factoring fee (100 000 CZK x 0.35% = 350 CZK) and funding interest (90 000 CZK x 60/365 x 2,6 % = 385 CZK)

So the factoring company will charge you a total of 350 + 385 = 735 CZK.

This means that overall factoring service cost is 0,7% of receivable nominal value.

Purchase of Receivables

The purchase of receivables means buying, funding, management and collection of short, medium- or long-term accounts receivable arising from deliveries of goods, services or construction work, usually for domestic customers. Purchases typically are of accounts receivable due within 180 days or longer. The eligible Receivables will have to meet certain criteria, that may differ depending on Factoring institution, nevertheless the general scope may be described to be following:

- it must be legally binding and freely transferrable obligation to pay

- resulting from ordinary business with max. payment terms (so not being overdue in a moment of assignment); further no Inter-company transactions

- not subject to any set-off or withholding etc.

- in agreed currencies and based on agreed jurisdiction.

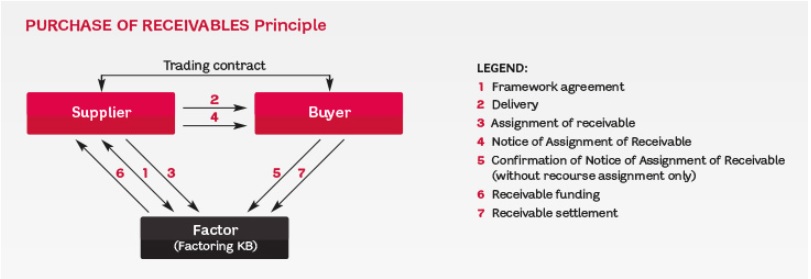

PURCHASE OF RECEIVABLES Principle

- Factoring Coy concludes a framework agreement on assignment of receivables for consideration with or without recourse to the supplier.

- Supplier provides goods, services or construction work to the buyer.

- Supplier assigns the account receivable while providing the necessary documentation to Factoring Coy.

- Supplier sends a Notice of Assignment of Receivable to the buyer.

- Buyer confirms the Notice of Assignment of Receivable (if the receivable has been assigned without recourse).

- Factoring Coy pays to the supplier funds equal to 100% of the account receivable’s value deducted by funding costs incl. Discount.

- Buyer pays the receivable in full to Factoring Coy’s account.

Costs Associated with PURCHASE OF RECEIVABLES

Depending on circumstances of a given transaction, the price for the purchase of an account receivable is agreed individually. As part of the transaction, the following items are invoiced to the client (i.e. supplier):

a) Factoring fee: includes cost connected with administering collection of the account receivable assigned to the factor.

b) Discount: a fixed rate (in % p.a.) derived from the reference rate valid as at the account receivable’s purchase date (like 3M EURIBOR) and increased by the factor’s margin.

The price for the assignment is usually set off against the nominal value of the assigned account receivable at its assignment date.

source: KB Factoring, Factoring Ceske Sporitelny, wikipedia.org