- A new accounting standard that will eliminate the distinction between operating and finance leases

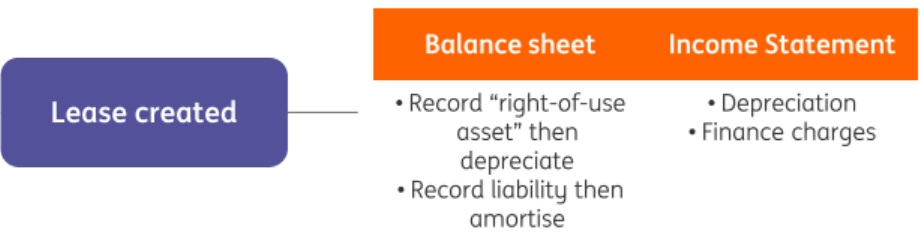

- A change in the definition of a lease to capture all assets identified as “right-of-use” assets, creating corresponding financial liabilities

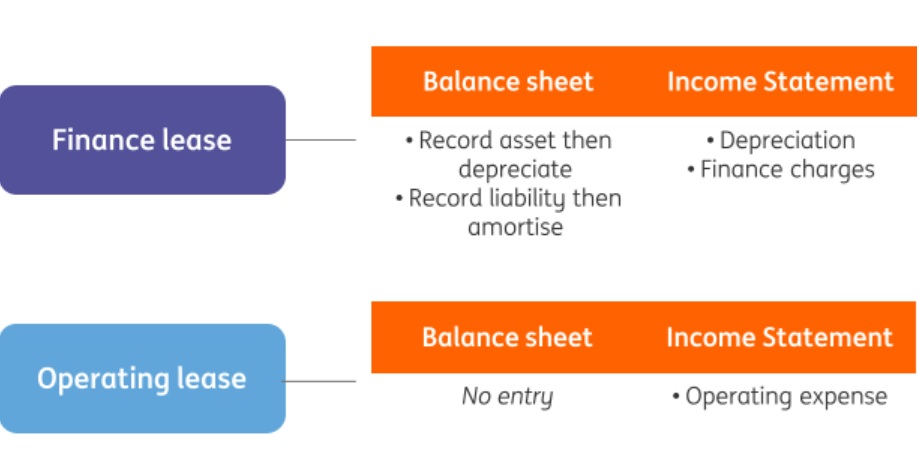

- After implementation, all leases will be accounted for in a similar way to finance leases today.

The reason why financial authorities and regulators adopted this new methodology is to make the financial statements of lessees more comparable to those companies that buy their assets funded via Bank loans or another On Balance-sheet instruments. This new rule is specifically targeting Operating lease, which was based on international accounting standards not recognized within the Liabilities as it was rather considered as a rental contract, so that lessee (the Client) accounted for rental costs within Income statement as another regular operating expenses. So that real intention is to provide greater transparency about a lessee’s financial leverage and capital employed, as for instance listed companies using IFRS Standards or US GAAP are estimated to have more than $3.3 trillion of lease commitments, of which 85% do not appear on the balance sheet.

Based on afore mentioned facts, it is widelly expected that newly adopted rules will have substantial effects on Corporate sector, whereas main financial parameters like EBITDA, Net Debt and naturally Leverage will be heavilly impacted. Below attached, please refer to estimated implications into base credit metrics of listed Corporates split into individual segments, according to Pricewaterhouse Coopers reaserch:

Whom does it affect?

- All companies reporting under IFRS

- Companies reporting under UK GAAP will continue to account in line with the current standard until expected alignment in 2023-24

- Companies reporting under US GAAP are not yet transitioning to IFRS 16.

So, the Implementation date was set for 1 January 2019 and Companies must report under IFRS 16 once a full financial year post-implementation is captured. This means that a company with a fiscal year ending 31 December will report in their FY19 accounts but a company with fiscal year ending 30 June would not report until their FY20 accounts (i.e. y/e 30 June 2020).

..and from Deloitte research:

“Research on 50 Dutch publicly-listed companies indicates that their combined net debt will grow by some EUR 45bn. This represents an increase in net debt of approximately 30%. We even observe that for 9 out of 50 companies, the increase of net debt is over 50%. We estimate a 13.5% increase in the average leverage ratio”

“The introduction of IFRS 16 should in principle have no impact on fundamental valuations, since the substance of the lease does not change the economics and cash flow generating capacity of the business. However, we expect that IFRS 16 will eventually impact the outcomes of valuations”.

Recognition and treatment of the lease

Old standard – IAS 17

New standard –IFRS 16

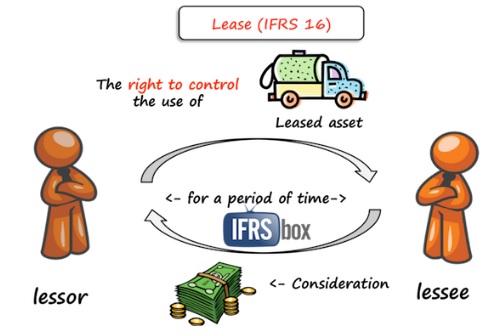

Conditioned with any lease contract, which conveys the right to control the use of an identified asset for a period of time in exchange for consideration (agreed payment). Control is defined as the right to direct the asset’s use and obtain substantially all the economic benefits from that use.

After the transition period, all Lease contracts will be fully captured in the Balance sheet (Liabilities) as well as purchased/ rented Fixed Assets, while the former one will be gradually amortized and the latter one will be depreciated with leasing payments. Next to the leasing payments incurred into Financial result of Profit and Loss statement, also Depreciation costs will be newly recognized.

Exceptions

There are some types of leases that are exempt from reporting under IFRS 16 and will continue to be accounted for as per the current regime (no recognition on balance sheet, lease payments recognised in line with the current basis).

Low value assets

- If the asset is considered low value, it is exempt from reporting. The suggested threshold for a low-value asset is USD 5,000, and is intended to capture Assets like laptops, phones, office equipment etc.

- Even if the combined number of low value assets becomes material (e.g. 100 x $4,000 laptops), they are still collectively considered low-value and thus out of scope of new IFRS16 rule

- Breaking down one large asset into many low value parts is unlikely to go unnoticed by auditors.

Short-term leases

- Defined as leases where the term is less than 12 months

- If the lease has an option to continue using after 12 months, the probability that this option will be taken should be considered – if it is considered likely, the asset is not a short-term lease

- Breaking a lease agreement into a series of 12 month contracts is unlikely to go unnoticed by auditors.

Companies reporting under US GAAP

- The US has not adopted IFRS 16 standards as part of US GAAP

- US companies reporting under US GAAP will continue to account for leases in a way in line with the current IAS 17 standard.

Impacted categories:

Valuations

Enterprise Value (EV) will increase but equity value will remain constant, implying a reduced equity cushion in all structures. A ‘new normal’ acceptable level of equity in a deal will have to be found over time.

During a transition period, the market will need to settle whether (i) the new Enterprise Values are acceptable to all capital structure participants at an increased level; or (ii) Enterprise Value is restored to pre-IFRS 16 values through a (gradual) reduction of debt in the system to adress increased Leverage/ gearing. A compromise position seems probable.

Ordinarily, an increase in leverage and a decrease in equity cushion would drive cautious investor behaviour and wider pricing. Some anomalies may arise post-implementation, however it is likely that bond investors will continue to rely on ratings agencies (who already assess companies on a basis similar to IFRS 16) and loan investors will receive sufficient information to “look-through” the accounting.

Ultimately, the standard will improve comparability and transparency as the EV/EBITDA multiples of businesses that own and businesses that lease assets become more aligned.

Structuring/ Credit analysis

CASH-FLOW Modelling

Current approach

- Operating lease expenses flow through the P&L as opex and are captured in EBITDA, which means that they are captured within CFADS and therefore on the numerator side of the DSCR metric

IFRS 16 considerations

- In P&L, operating lease expenses split into depreciation and interest (both below EBITDA)

- CFADS will increase due to higher EBITDA, but the actual cash spent on leases is unchanged. The cash payment moves from opex to financing flows below CFADS. Net cash flow is unchanged

- Payment holidays and other items that delay or bring forward cash payments on operating leases will be an adjusting cash item

Conclusions /recommendations

- Cash paid on operating leases will remain the same as before IFRS 16. Actual cash payments should be included below EBITDA (as interest or split of interest + principal – shown opposite), which will impact DSCR in following ways: (i) running the entire lease payment through as a single cash item above CFADS (Cash flow after Debt service) is simple and results in no change to DSCR (ii) however, moving the cash lease payment above CFADS undermines our interest cover metric, which is based on EBITDA / cash interest (not P&L) or (iii) a solution would be to include a separate calculation with cash lease payments above CFADS to reconcile to pre-IFRS 16 DSCR.

PL Modelling

Current approach

- Operating lease expenses flow through the P&L as opex and are captured in EBITDA giving well understood interest cover and refinancing risk metrics and EBITDA profile

IFRS 16 considerations

- EBITDA and total balance sheet debt will both increase

- Depreciation of the right-of-use asset is charged to the P&L in the same way as the company’s existing accounting policy

- The interest expense in the P&L steadily reduces over the course of the lease tenor and the capital repayment portion (i.e. the reduction of the balance sheet liability) increases correspondingly

- P&L timing differences between depreciation and interest cause a difference at net profit level

Conclusions / recommendations

- Changes to depreciation should be considered when taking into account capex vs. depreciation analysis

- For tax interest deductibility purposes, rules are broadly the same

- SAF’s interest cover ratio is based on EBITDA / Cash Interest, so does not necessarily need to be impacted by the P&L interest vs capital allocation. A simple approach would be to consider the entire interest + capital cash amount as ‘interest’, although this could result in materially different ratios

Legal docs

Most recent documents have the concept of ‘Frozen GAAP’ included, which mean that nothing should change in terms of measurement – EBITDA, cash flow and debt will still be calculated in the previous way so will not affect any debt or EBITDA dependent metric. Nevertheless, at some point, it will be necessary to transition to IFRS 16 financial metrics and update documentation accordingly. The most likely flashpoints in documentation under the new standard will be as follows:

- covenants (leverage, interest cover, fixed charge cover)

- ratios tests based on EBITDA / cash flow or assets (including guarantor coverage tests, equity cures etc)

- baskets/ agreed thresholds – e.g. Permitted Indebtedness, Allowed Payments etc.

Ratings assessment

“The new IFRS accounting will closely mirror S&P’s existing approach”

- Post-IFRS 16, Moody’s will use the issuer’s own calculated lease liability (since IFRS 16 accounting treatment is considered to be in line with Moody’s approach). This may result in a different amount of liability vs. what was recognised historically. As per Moody’s, S&P will use the issuer’s own calculated lease liability in its analysis in most cases

- Also as per Moody’s this could result in a different liability amount recognised (especially given S&P’s current standard 7% discount rate used to calculate the PV of lease liabilities, which they note may be too high in the current low interest rate environment)

- The post-IFRS 16 income statement and cash flow is largely per existing S&P methodology: (i) S&P will continue to allocate the lease-related expense to interest and depreciation on the Income Statement (ii) S&P will continue to reclassify cash interest on leases as an operating cash flow (a different approach to Moody’s who reclassify the cash flows to investing and financing flows).

- S&P do not intend to modify their ratio benchmarks, noting that even if a change in ratio results in a downgrade to the Financial Risk category, there is sufficient flexibility and analytical judgment to enable credit analysts to arrive at the appropriate credit rating.

ECB measuring

Key ECB requirements impacted by IFRS 16 are:

1) “Highly Leveraged Transaction” definition: Total Debt to EBITDA >4.0x at deal inception. Deals >6.0x should be exceptional.

2) The definition of Total Debt used in this calculation could potentially include all capitalised leases post-IFRS 16. However, consistency of approach should take precedence over accounting changes to ensure comparability and transparency in our reporting to the ECB.

3) It is proposed to exclude capitalised leases from our definition on this basis, to be revisited if further guidance is received from the ECB on how they would like lenders to address the IFRS changes.

4) Whilst capitalised lease debt is to be excluded, Permitted Indebtedness baskets are included in the leverage calculation per individual Banks policy, and this includes baskets for lease debt. To the extent that lease debt carve-outs are increased to allow the borrower to retain existing operating leases and provide flexibility to enter into future “operating leases”, this will be captured in the ECB leverage calculation and further increase Total Debt to EBITDA.

This test affects regulatory reporting as well as more deals will surpass the 4.0x / 6.0x threshold, meaning more transactions will be reported to the ECB being Leverage finance transactions.

5) Repayment Capacity: a leveraged borrower must fully amortise at least 50% of Total Debt over a maximum period of seven years.

As per Test, capitalised lease debt should be excluded from the Total Debt to be amortised, to drive consistency and comparability in Banks reporting. In addition, it seems reasonable that leases are excluded from this aspect of the calculation given that (i) lease debt relates only to specific assets so lease lenders do not have a claim over the entire business, presenting a different risk / recovery profile to term debt; (ii) leases may have tenors longer than 7 years so should have longer to amortise; (iii) lease agreements will most likely be on materially different terms to the term debt and may include break clauses, rights of substitution and otherwise greater flexibility that make the amortisation requirements less relevant. So that, as part of any analysis of Permitted Indebtedness, attention should be paid to any increases to leasing baskets driven by IFRS 16 implementation, which will feed in to the Total Debt to EBITDA reporting test above.

sources: www.ifrs.gov, www.iasplus.com, www.pwc.com, www2.deloitte.com, www.ecb.europa.eu