Lending activities still dominate on core-business of financial institutions and banks, especially in terms of their Balance sheet and Income structure, as they account for more than 50% of Assets and generate major part of Interest income. This structure may slightly differ when it comes to Investment banking or Specialized lending vehicles, but speaking about commercial banking this assumption remains valid.

Investment banks on the contrary generate higher income from their trading activities, from FX and Derivatives operations and from Bonds (LT-holding and/or ST-trading), while specialized lending institutions like Leasing companies or Brokerage companies receive mainly Interest or Fees-related revenues from their core products.

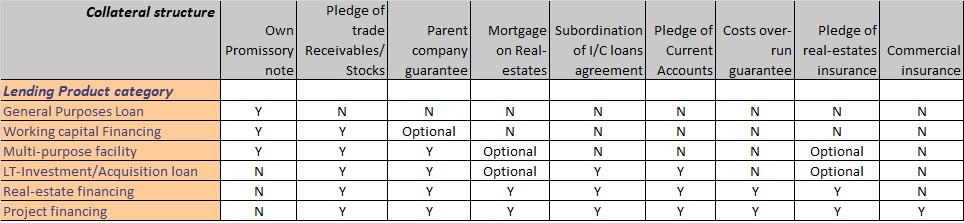

Back to commercial banking, the Lending products (for Corporate clients) will be further depicted in this Section for better understanding of:

- How are various products structured

- What are the main collaterals to cover the risks

- What is the usual documentation type for such products.

Below attached picture provides overview on complexity of various products in ordering from the simplest one to most complicated.

The scope of lending products provided to Corporate clients is pretty much linked with Clients segmentation in the Banks, which leads then to standardized legal documentation which is usually tailor made for Clients with different knowledge and expertise on transaction structuring, legal environment etc. Each Bank keeps on developing its own legal documentation (drafted by in-house Lawyers), which is beneficial especially in cases when:

- better control on Clients development is needed thus imposing some additional conditions and covenants;

- higher alignment with Group policy is required to secure easy transferability of problem loans onto Head-Office which is then engaged in Work-out activities and bad loans management;

- requirements of law, regulators and external Auditors to be swiftly implemented.

The internally drafted legal documentation provides usually basis for negotiation in case of more plain-vanilla transactions like General purpose loans, WCF and Multi-purpose facilities, that are provided to clients from segments like Micro-clients, SME clients and MidCorps. While on the contrary, LargeCorps resp. Project finance entities and REF SPVs are more experienced with more structured documentation that is LMA based. For additional information on LMA documentation, please refer here.