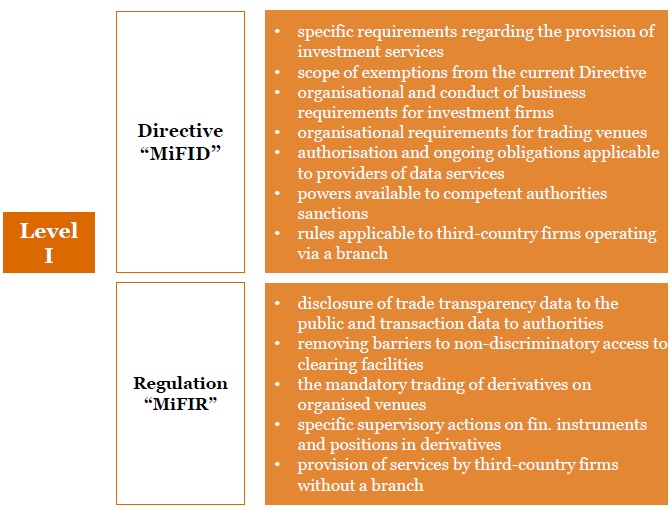

The Markets in Financial Instruments Directive (MiFID) has introduced a single market and regulatory regime for investment services across the 31 member states of the European Economic Area (EEA: the 28 Member States of the European Union plus Iceland, Norway and Liechtenstein). There are 3 objectives to be met by the Directive:

1) to complete the process of creating a single EU market for investment services

2) to respond to changes and innovations which have occurred in securities markets

3) to protect investors by making markets deeper, more competitive and more robust against fraud and abuse.

New MIFID regulation has replaced the previously applied Investment Services Directive (Directive 93/22/EEC).

MiFID applies to locations in the EEA where a MiFID service is offered or provided i.e. the sales relationship (legal entity and location of trader are not determining factors) or where the client is based in the EEA. As such, if a Singapore-based Banks salesman sells a MiFID product to a Singapore corporate client, which is then booked in the name of Deutsche AG London Branch (due to Global Product line within the Organisation structure of the Bank), this transaction is outside the requirements of MiFID. However, if the client were based in the EEA then MiFID would apply. (Note for transaction reporting it has been agreed that the approach will be based on legal entity, so Singapore initiated deals booked on Deutsche AG London accounting records, it will be included in London transaction reporting). The same logic would apply with a salesperson in Singapore where the price is obtained from a trader in London.

Under MiFID, clients are assigned to one of three categories:

a) Retail Clients

b) Professional Clients

c) Eligible Counterparties (ECP)

The MiFID Retail clients category is the classification that offers the most protection and imposes the most requirements in terms of communication, disclosure and transparency. Retail clients are clients that do not belong to the Professional or Eligible counterparties categories.

Professional clients include entities not classified as Eligible counterparties, which are authorised or regulated to operate in the financial markets, such as credit institutions, investment firms, insurance companies and pension funds.

This means that clients that could otherwise be classified as an Eligible counterparty are categorised as Professional clients if the investment services they receive do not involve the reception and transmission or the execution of an order.

Large undertakings can also qualify as Professional clients if they meet at least two of the three ‘large undertakings’ criteria:

1. Balance sheet total of at least EUR 20 million

2. Net turnover of at least EUR 40 million

3. Own capital of at least EUR 2 million.

Under MiFID rules, Professional clients need to provide less information to their financial institution than Retail clients. In return, they receive a lower level of protection than Retail clients.

An Eligible counterparty (ECP) is an entity that is authorised or regulated to operate in the financial markets that is not given investment advice.

An Eligible counterparty (ECP) belongs to one of the following categories:

a) Investment firms

b) Credit institutions

c) Insurance companies

d) UCITS and their management companies

e) Other financial institutions authorised or regulated under Community legislation or the national law of a member state

f) Commodity dealers and ‘locals’ on exchanges

g) National governments and their corresponding offices, including public bodies that deal with public debt

h) Central banks and supranational institutions.

If such clients are provided with investment advice, they will be treated as Professional clients instead. ECPs receive the lowest level of protection under MiFID.

Sources: www.ECB.Europa.eu, www.ft.com, www.pwc.com