October 2019 has become another milestone for a banking industry, as gradual phase-out process for its reference benchmark rate(s) has just begun. For more than 40 years in a row, the financial institutions world-wide have been using the floating market reference rates like LIBOR, EURIBOR, EONIA etc. for determining the interest costs of credits, bonds, mortgages, deposits, repos and other products in various currencies (USD, GBP, EURO, CHF and JPY mainly – all these rates are collectivelly called as IBOR rates). This means, that if any banking product was priced at floating rate, its total interest rate was derived from those market reference rates depending on tenor and currency of each product. Further, these market rates are still used to calculate the current market value of derivatives and as a tracker for certain investment funds performance etc. Nowadays, around 350-370 trillions of U.S dollars in securities and loans are linked to USD Libor, including over half of the United States’ floating-rate mortgages.1

The history explained

So, when this system worked well for more than 40 years, why there is a need for a change? Basically, two major factors have been taken into consideration for such a big move towards the more transparent and robust rates:

- All IBOR-related rates have been set during the panel-consensus by money market dealers who contributed daily their Bid/Offer rates for a forward looking period (overnight, tom-next, 1/2/3/6/12 month etc.). Inter-bank broker then stripped off the lower and higher quartills and remaining values served for computing the average rate thereof. This mechanism was intended to prevent from any manipulations, howeveras it was recently revealed, some participating banks and brokers were in fact rigging the rates for a couple of years.

- And further, these dealers contributions (quotations) were supposed to indicate their expectations for borrowing costs, but without particular underlying transactions. This enabled them to keep the market rates artificially lower if needed, even during the market turbulent period after the year 2008 and so, despite the fact that emerging markets faced market disruption for certain period. This is quite opposite to bilateral rate quotation between two entities, when providing the rate „off the market“ can result to direct financial loss, while pannel quotation through a broker does not result to borrowings at unfavorable costs, as it only pulls down the resulting average rate, which then serves for direct price setting mechanism on a interbank market.

In fact, most famous person who was found guilty with respect to having played the central role in this financial scandal, was Thomas Hayes, an former money market dealer, who used to work for Barclays, UBS and Citibank in different years. UK Court finally sentenced him for 14 years in prison due to fact that his rigging activities were aimed for his personnal benefit out of it. Below attached is a picture of Mr. Hayes leaving the Court.

After the international investigation led by U.S. and EU regulatory bodies like Commodity Futures Trading Commission (CFTC), UK-based Serious Fraud Office (SFO), U.S. Department of Jusitce (DoJ) and others confirmed that many dealers were in collusion, couple of major market participants including Barclays, RBS, UBS, Deutsche Bank, JP Morgan, Citibank, Societe Generale and Rabobank were fined with total penalties over USD 9 billion for LIBOR manipulations, since then European regulators and other governing bodies started to work on reforming the IBOR. 2

In 2012, UK parliament passed the legislation to stregthen the market regulation. As a consequence, a new government agency, Financial Conduct Authority (FCA) with centralized and expanded powers to investigate and regulate financial markets, was established. This was the very first step for further LIBOR transformation. Later, the Financial Conduct Authority shifted supervision of Libor to a new entity, the ICE Benchmark Administration (IBA), an independent UK subsidiary of the private exchange operator, Intercontinental Exchange (ICE).

Though the Libor mechanism was kept in place for existing contracts and new contracts were allowed to use either Libor or a transaction-based benchmark rate until the ongoing reforms of the system are completed, the gradual phase-out proces for LIBOR and other related rates has started. All those concerns about LIBOR transparency led to recommendation made by Financial Stability Board (FSB) in 2014 to reform reference market benchmarks and to implement near risk-free rates (RFRs) based on liquid over-night lending markets instead of IBORs.

Where we are now?

Since 2nd October 2019, the transition period was launched as new alternative reference rates have started to be used along the traditional IBOR rates, which are widely expected to be discontinued around the end of year 2021 based on agreed consensus with panel of Banks. However, as it was indicated by Andrew Bailey, chief executive of FCA, the panel banks are getting more reluctant to continue in regular contribution to reference benchmark rates for longer period (originally the IBORs were supposed to continue for another 5 years). To demonstrate the problem, FCA was facing, one of the interest rates being set was based on submissions from a panel of banks, which only conducted 15 relevant transactions in the whole Year of 2016.3

To create more robust alternative rates, international regulators and working groups have been designing new process, how the rates will be computed to become free of any manipulation risk as well as free of any credit risk (premium), as both risks are in fact incorporated in current IBOR rates. And to achieve these goals, the structuring of the rates has changed in following way:

- vast part of reference rates are expected to be moved from unsecured to secured (repos) borrowing transactions,

- the calculation of Over-night alternative rate in EURO currency (ESTR) will come from realized transactions on the previous day (D-1), which is in the contrast to „forward looking“ fixing of IBOR-related EONIA, currently set for upcoming period (D+0).

This is the short description, how it works in case of European rate:

1) ESTR rate published daily 7 a.m. London time for previous day fixed rate Over-night deposits with notional amounts exceeding EUR 1 mio each,

2) European Money Markets Institute (EMMI) publishes Eonia using the new methodology at about 8:15 a.m. London time,

3) Eonia (EU Overnight index average) to be set at ESTR plus a fixed 8.5 basis surcharge.

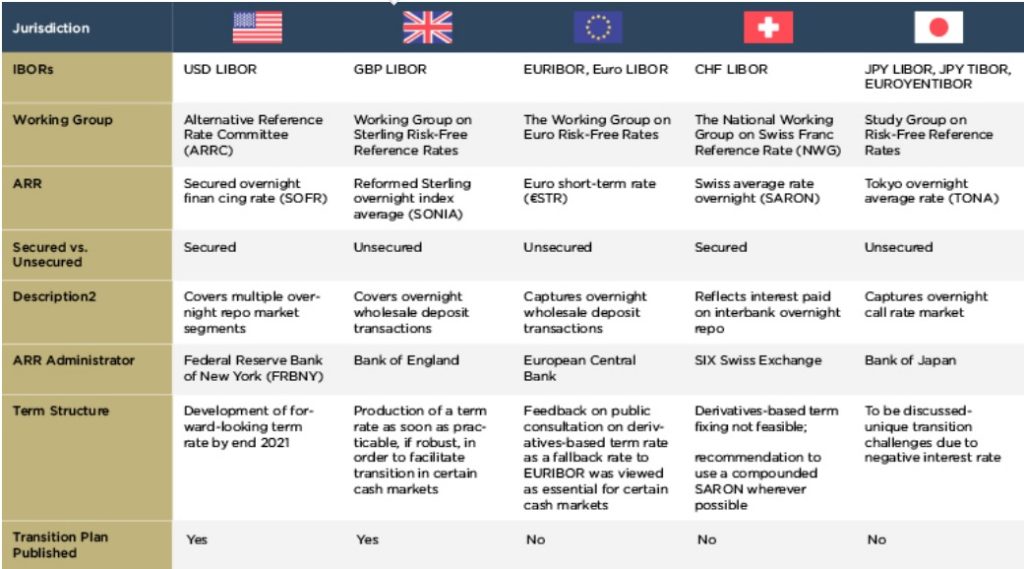

Below attached is the overview of current market reference rates, that are undergoing this transition, however only major currency rates have been listed. Another currency rates that will be affected as well include Australian BBSW, Hong-Kong HIBOR, Singapore-based SIBOR etc.

The Present and Future of market rates

The very first ESTR fixing for 1st Oct. 2019 resulted for -0,549%, and it was based on a volume of almost EUR 36 bln completed between 32 banks in 432 transactions, the ECB said. The share of volume from the five largest banks was almost 54%.(4) Although the European reference rate has been slightly behind the U.S. rate in transitioning process, the transition from Eonia to ESTR should be pretty straightforward, given the fact that Eonia is to be newly derived from this alternative rate (ESTR). For a better coordination of market participants in case of any market disruption and for future decision making, ECB issued together with its Working group the Report on risk free Euro rate in November 2019, see below attached.

On the contrary to that, SOFR an alternate rate to USD LIBOR, which U.S. Fed started to publish in April 2018, had to be created nearly from scratch. Nevertheless, the U.S. (and UK regulators) were quite successful in convincing the market participants in using these new reference rates, so that in 2018 on U.S. market there have been already more than 30 Forward rate notes issueances, which were priced on SOFR. In addition, the Federal Home Loan Bank entities replaced LIBOR with SOFR in November 2018. And FASB gave SOFR an Hedge-accounting status as reference rate for revaluation purposes.

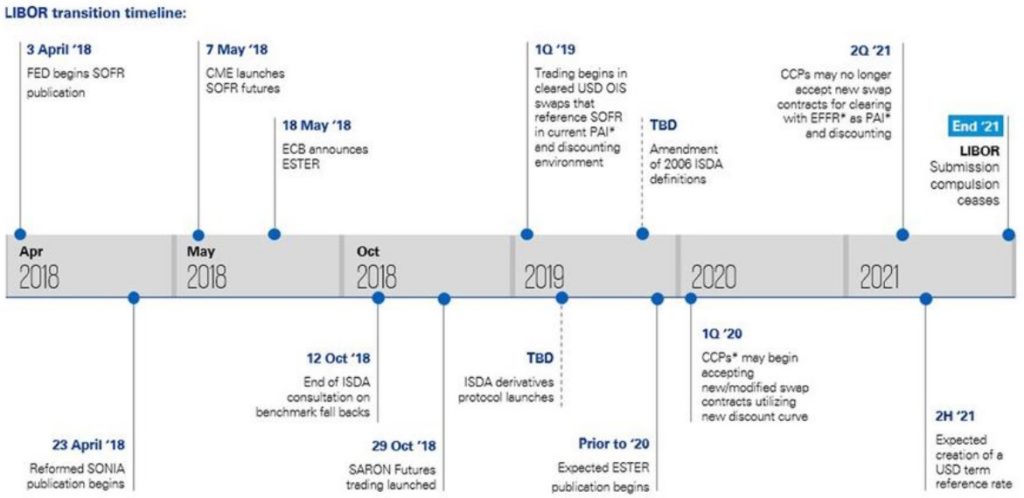

Also, in UK financial market, there has been significant increase in „reformed“ SONIA linked Bonds (with maturities up to 5 years) issuances, which are expected to reach and exceed GBP 10 bln in 2019, itself. More important for Derivatives market is the fact, that SONIA/LIBOR swap market was well established as well. For a future period, LIBOR is still expected to become the third benchmark rate used under no-deal BREXIT situation. And naturally, SONIA futures rates are yet to be developed. Below attached is the expected timeline for transition process:

Implications on financial industry

- Loan documentation and ISDA adjustments to make reference on new alternative rates resp. to implement „Fall-back“ procedure for worst case if the originally concluded rate is not available on market

- Hedging accounting – redesigning the model curves based on a new rates; CSA documentation to be aligned with new alternative rates

- IT systems and reporting – to be updated for capturing the new rates for funding costs

- Controlling issues – calculation formulas within Profitability section of the Banks

- Assets and liabilities management – matching the funding costs with interest revenues to cover the potential gaps

- Commercial activities – proper pricing setting needed for offered products

- And others

Unknown Issues

It’s not clear if the ECB’s recent move to apply negative rates differently among various banks, known as tiering, will affect ESTR. Tiering came into effect on Oct. 30th 2019. Further, as ESTR is calculated as a weighted-trimmed average, the impact of new flows will depend on their size relative to the volume of transactions that are eligible to calculate ESTR, so question is whether these new bids will go on top of existing ones or will crowd out less attractive bids. And finally, the newly applied ESTR is coming out of previous days transactions volume and is expected to replace EONIA rate, but still certain hybrid methodology has to be elaborated by EU working group on how will be EURIBOR newly computed for so called „forward-looking“ period like upcoming 1-Month, 3-Month etc., to become fully EU Benchmark Regulations “BMR” compliant (the base requirements can be described as sufficient volumes traded in recent history and written scenario for a situation that the rate ceases to exist). For instance, term reference rates on U.S. Dollar borrowings are expected to be applied based on SOFR Derivatives in 2H 2021.

Conclusion

IBOR transition can be for sure recognized as one of the major regulatory projects in banking industry in latest decade, which will have huge impact on all areas of banking activities and will create new platform of funding and commercial functions. To demonstrate the importance of these changes, this is the part of the statement from FCA executive Andrew Bailey: “I hope that it is clear that discontinuation of LIBOR should not be considered as remore probability of Black swan event. Firms should treat it as something that will happen and they must be prepared for it.“ 5

Sources: www.theguardian.com, www.bloomberg.com, www.cfr.org, www.nytimes.com, www.gbm.hsbc.com, www.fca.org.uk, www.accenture.com, www.kpmg.ch, www.simcorp.com

References:

1/ Understanding the Libor Scandal by James McBride, published in October 2016 2/ Notes on a Scandal: The Story of the Libor Financial Scam by William D. Cohan, published in April 2017 3/ Libor scandal: the bankers who fixed the world’s most important number by Liam Vaughan and Gavin Finch, published in January 2017 4/ ECB Begins Transition of Benchmark Short-Term Interest Rate, By Liz McCormick and James Hirai, published in October 2019 5/ Interest rate benchmark reform – transition to a world without LIBOR, by Andrew Bailey, published in July 2018

Update

ECB published in October 2020 an publication on financial industry response to envisaged compounded rate mechanism for ESTR computation. Based on this publication, the following conclusions have been made:

- The vast majority of respondents are in favour of the ECB publishing a compounded ESTR-rate. The ESTR compounded rates are expected to be reliable and robust as the calculations would be based on the overnight ESTR.

- Most respondents supported the analyses and conclusions as outlined in the consultation paper, and agreed with the proposed day-count convention. It was acknowledged that the modified previous business day convention seemed to be the most accurate option for backward-looking compounded term rates, as the

occurrence of timing mismatches would be reduced compared with the modified following business day convention. - The proposed selection of maturities received wide support because it is aligned with current standards and euro interbank offered rate (EURIBOR) maturities. As for non-standard tenors, the proposed index values could be used for calculating interest.

- This would facilitate the usage and adoption of the ESTR com-pounded term rates for both new and legacy contracts as possible fall-back provisions.

- Most respondents perceive the index as a simple and transparent solution for managing non-standard tenors and broken interest periods, as it enables maximum flexibility. It was mentioned that the complexity of the compounded rate calculation is manageable and transparent.

the full text is herewith attached: