Considering the (Government Bonds, Mortgage loans) Yields or interests, the global investors encompassing the Banks, Assets Managers, Pension Funds, Insurance conglomerates etc., they all arguably need to assess following aspects, when trying to target higher returns from their investment:

- Spreads between the Bonds issued by different Issuers and Countries (like US T-Bills, German Bunds or Czech Government Bonds

- Spreads between the Bonds of same Issuer, but on different tenor whereas the LT-ones (30 Years) usually bear higher Yield than ST-one (10 Years). In case that market conditions lead to situation that ST-debts are priced with higher rate than LT-one, then it is referred to Inverted Yields curve.

Afore attached chart shows Spreads on 10-Year Government Bonds issued by highly developed countries. What is quite clear from this comparison, the US debts seem to generate highest return (around 2%), while among the EU countries the similar Yield can be expected only on worse performing countries like Italy or Spain, while UK or Germany sovereign debts carry negligible yields around zero.

And even, during the 2Q19 the Greece has also joined other Issuers from European Union (like Italian, Portuguese, Spanish) to offer the Yields comparable to US debts. Yes, on 3- and 5-year bonds, Greece, with its rating deep in junk territory, pays investors less than the AA+ rated U.S. government does.1 And this is just shortly, after it has successfully exited the ELA bail-out programme, which means that is has narrowly escaped from state bankruptcy.

This single comparison raises couple of questions. Does it mean, that given the similar yields on their sovereign Debts, is the Greece’s government in fact, as creditworthy as the U.S. government? Or, should global investors focus on higher yields from the U.S. bonds? And why are they willing to accept the even lower yields on the bonds of other eurozone governments?

So, lets imagine that an EU-based asset manager, who has liquidity excess in EUR, seeks for an alternatives, where to invest free money in order to gain solid yields and returns for his Fund stakeholders. Therefore, following investment opportunities can be considered:

- Investing into Investment-grade EUR Bonds (Germany, Denmark, Sweeden, Austria, Norway, Czech Republic etc.): such investment will generate perhaps very low interests, if not negative, depending on specifically purchased paper (and when it was issued). So that, investor will not benefit from Yields, but still can make some profit from changed Debt paper market price, which is however unsure. The Yield is always fixed on the issuance date, so that it represents “guaranteed” income on investment, while the price itself tend to oscillate given the market trends. In this case, the price movement can be still positive, when market participants will anticipate that market rates on EUR funds will decline further in line with monetary policy of ECB, so that will do also the Yields on newly issued Bonds in future and therefore they will try to purchase from market these Bonds with existing Yield (even though with zero rates). So that, the profit could be potentially achieved, only from sale of Bonds, when their market price was above the face value (above par), which might or might not happen. And further, when considering 10 Years investment and to beat the investing option No. 2 with secured 2% annual return, the market price should increase by 20% in 10 years, at least, which is the big lottery given the constantly changing monetary policy of central banks in 10 Years horizon.

- Investing into sub-Investment grade EUR Bonds (Italy, Greece, Spain etc.): this investment represents more risky alternative to option 1, despite the fact that Investors are guaranteed with fixed annual income of around 2% when holding such Bonds. Nevertheless, as mentioned previously, this is connected with higher sovereign risk, so that potentially the Bonds could not be repaid at their maturity or they might be subject to restructuring, like it was the case of Greece Debt papers some 5 years ago. And this is quite likely to happen, as these countries are typical for higher political instability, higher public debt (around 150-200% of national GDP), more fragile banking sector and weaker performance of domestic economies.

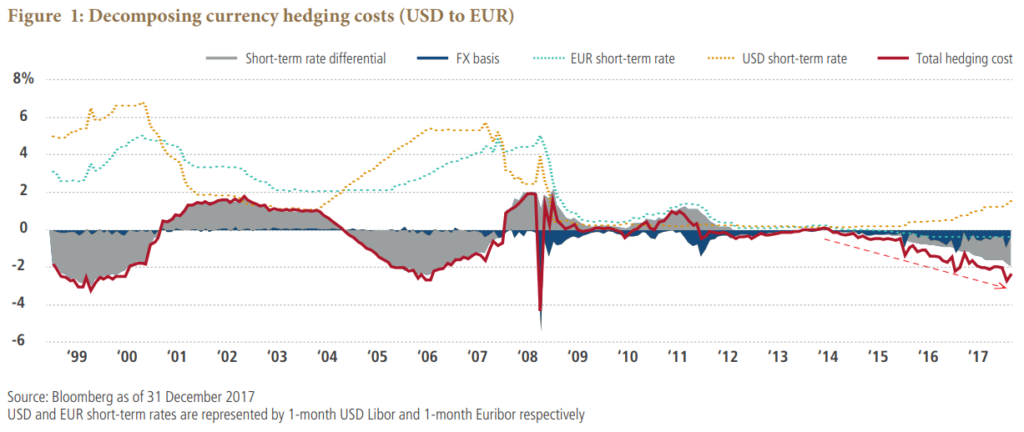

- Investing into U.S. T-Bills: this option will bring certainly higher interest income, as the Yields from U.S. Paper debts are priced above all European countries; further investment into U.S. Government debt is always considered as safe heaven. Therefore, such investment is supposed to be repaid, almost for sure. However, it is not a risk-free alternative, as FX-risk must be considered in this case. An EU-based investor has to convert EUR funds into USD to be able to purchase U.S. T-Bills. Then, the question is, how much EUR funds will be again received, after T-Bills maturity date and when selling USD back to EUR. Quite simply, when there is a global trend of buying USD assets, it is connected with higher demand for this currency, so that mutual EUR/USD rate will weaken in favor of USD, in a future. So, that in order to protect against this risk, the Investor must take into consideration also the hedging costs into the final result of this investment. And very much, the FX forward/swap rates very often reflect these Yield spreads in their construction, so that it is the zero-result game, in the end. For instance, during the 1H19 the Yield spreads between U.S. T-Bills and 10 Year German Euro-bunds made in average 250BPS, while corresponding hedging costs between USD and EUR ranged between 270 and 325BPS.2 For instance, see below attached graph of historical decomposition for currency hedging costs in period 1999 – 2017.

Quite clearly, potential future spreds must be considered by local central banks when calibrating the rates and monetary policy. For instance, faster eurozone growth would likely come with increasing inflationary pressures, which in turn would lead the European Central Bank to raise its policy interest rates. The higher short-term interest rates and more attractive investment opportunities accompanying the pickup in growth would suck money into the eurozone, thus raising the euro’s single-currency value.

Bonds Yields are important indicator of expected future development of domestic economy, so that their development is closely followed by all market participants. This is mainly due to the fact that, monetary policy set by central bank very often targets potential inflation rate, so that the yields on ST-state papers, which further imply on ST-bank deposit rates, should secure at least small return from placing the free liquidity in those products, and that above the current/future inflation rate. The willingness of investors to undertake also the LT-horizon risk and to invest into 10, 20 or longer debt papers should be naturally rewarded with higher return, so that the longer „tail-end“ yields should be higher under normal circuimstance.

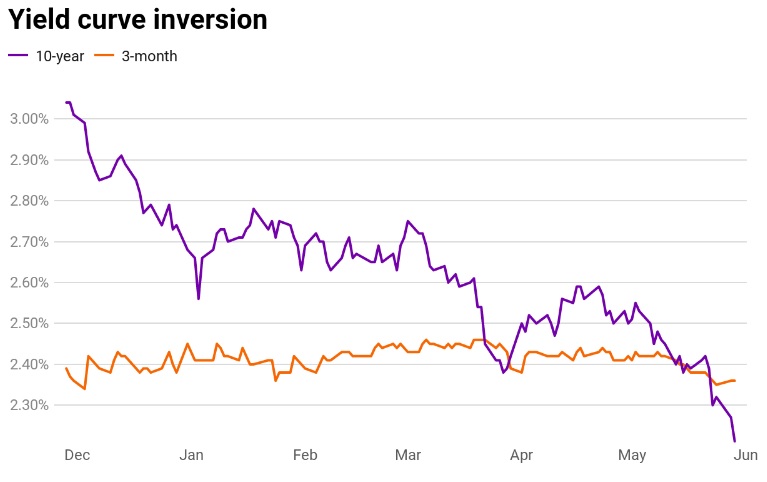

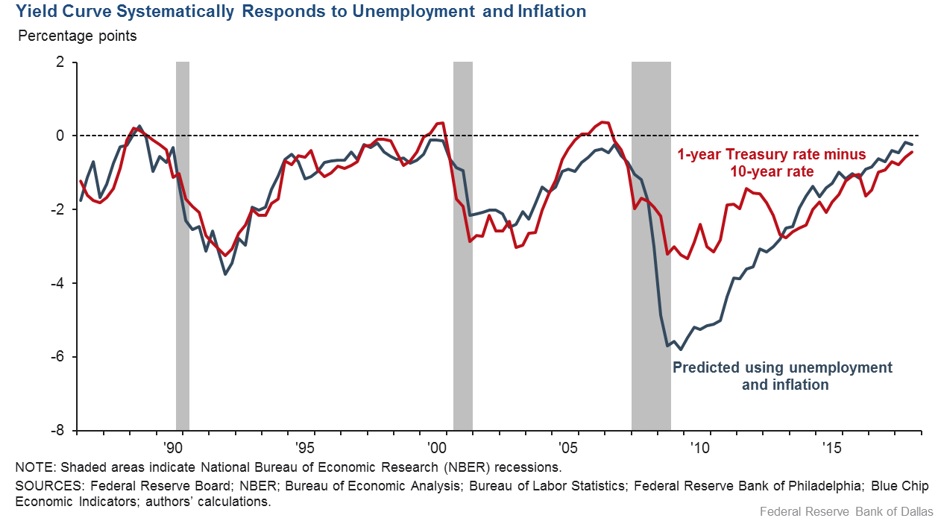

Above attached chart shows the development of U.S. T-Bills yields on different tenor during the 1H2019. Such situation, when for instance Yields on 10 Year Bonds fall below the 3 Month T-Bills, is very often addressed to be pointing out to coming recession on the market, as it means that investors are more worried about the ST-horizon of Issuer sovereign risk, while over the longer period, they still believe that performance of economy will „normalize“. That is connected with previous experience from the past, when shortly after the inversion took place, the unemployment followed by inflation went higher. Generally, as the gap between long-term and short-term interest rates narrows, even small policy moves may suddenly have a larger economic impact than before.3

Such situation may be dire for all market participants, especially banking sector is known for funding its LT-lending activities from ST-deposits thus creating „liquidity“ gap, but this is quite an industry standard as obviously, there is very low interest of customers to pledge their savings with bank accounts for a longer period. Having said that, the situation of inverted Yield curves translates into profitability issue as well, as Banks will have to raise interests offered on ST-deposits, while their income from LT-loans will be lower. Quite clearly, such situation can not be sustainable for a longer period to last.

Further, the Governments and States that are used to heavilly finance their public deficits through Bonds, may have found such market conditions quite tricky to roll-over their maturing debts with a new one and under increased Yields. This naturally increases the costs for debt service, as ST-papers are placed on market to manage the current liquidity of public budget, and to cover sudden shortage in cash. As the funding costs for public debt represent quite important measure also for a rating agencies when assessing the sovereign rating of Issuers, no Government wishes to stand such situation.

And, finally, the consumers and investors get confused, when they judge whether to re-allocate their savings from LT-bonds and Money market instruments into ST-deposits, when chasing for better returns and thus creating instability in banking and financial segment.

sources: www.cnbc.com, www.pimco.com, www.federalreserve.org, www.reuters.com

References: 1/ David Reid: „Greek 10-year yield dips under 2% for first time ever, back below US 10-year“, dated July 2019 2/ Andreas Steno Larsen: “USD Hedging costs may have peaked”, dated April 2019 3/ Karren Brettell: “U.S. Yields curves inversion highlights recession fears, FED dilemma”, dated August 2019